KEY MARKET MOVES

MACRO OVERVIEW

Global

Angst surrounding the global banking crisis sapped overall risk sentiment, pushing equities lower on Friday. Concerns surrounding the banking turmoil may tip the economy into recession.

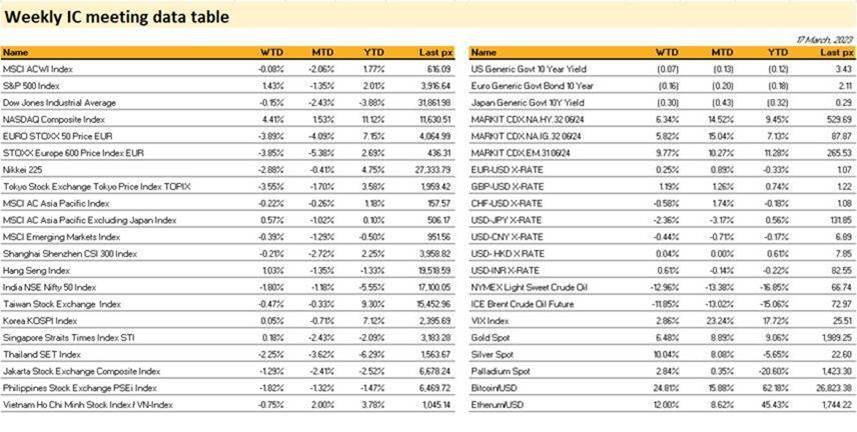

Despite the volatility, US markets ended in the green as Treasury yields continue to tumble, with the UST10’s at 3.428% and 2’s at 3.837%. The Nasdaq capped its best week since November finishing up 4.4%.

Financial stocks were the biggest drag even as cash infusion to First Republic Bank was seen as insufficient. Additionally, the Fed said it stands ready to provide liquidity through the discount window to all eligible institutions.

The ‘higher for longer’ narrative by the Fed led analysts to opine that there’s possibly more skeletons in the closet for other banks.

This week’s FOMC meeting will be eyed particularly closely as the economic outlook has been clouded further. A likely outcome now could be a pause in its tightening cycle. Consensus remains for a 25 bps hike in the Fed Funds rate to 5%.

This comes hot on the heels of a cooling inflation release, which saw CPI YoY headline falling to 6% from 6.4% previously and the core rate to 5.5% from 5.6% ~ all within expectations. PPI showed a higher dis-inflation pace with the YoY core coming in at 4.4% vs views of 5.2%. Retail sales came in lower than expectations ~ all of which may have given the Fed some breathing room. The U. of Mich. 1 yr inflation expectations fell to 3.8% with the 5 yr also falling to 2.8%.

Contagion risk is the main headwind as we approach the week with Credit Suisse being the focal point. Holders of Credit Suisse Group AG bonds suffered a historic loss when a takeover by UBS Group AG wiped out about 16 billion Swiss francs (USD 17.3 billion) worth of risky notes. The deal will trigger a “complete write-down” of the bank’s additional tier 1 bonds in order to increase core capital.

In a case of “told-you-so” cryptos enjoyed a rare rally following the banking turmoil. The alternative block-chain infrastructure held up firm with ETH trading at $1800 and BTC breaching $27,500 for the 1st time since June 2022. Crypto-exposed stocks also outperformed on US agencies’ pledge to fully protect all SVB and Signature Bank depositors.

We see opportunities in some growth sectors as LT yields continue to slip. AI-chat Tech appeals.

Asia

China markets have notably underperformed following early-year rally driven by reopening momentum. Latest selling a function of deterioration of risk appetite from recent global banking issues. Disappointing earnings out of Hong Kong, lack of meaningful stimulus signals from NPC, and ramp in US-China tensions also blamed for market malaise.

The PBOC net drained CNY983B ($141.09B) this week, the most in more than two months as liquidity requirements loosened at the beginning of the month. It is the fourth consecutive week the PBOC has withdrawn liquidity in open market operations, and the biggest since the first week of January.

The PBOC delivered a surprise 25bp RRR cut, to lower the average reserve requirement ratio of financial institutions to 7.6%. This is expected to release ~RMB500bn of liquidity into the system, a sign that China’s economic policy will remain accommodative to facilitate the growth recovery amid muted inflationary pressures.

China’s leader Xi Jinping on Monday vowed to bolster national security and build the military into a “great wall of steel,” in the first speech of his precedent-breaking third term as president.

In geo politics, US and allies unveil submarine deal to counter China in Pacific. Under the AUKUS agreement, which is aimed at preserving a “free and open” Indo Pacific, Australia will buy three American nuclear submarines.

India’s retail inflation eased in February. Prices are still higher than the country’s central bank wants, meaning rate hikes are likely on the way next month.

Japanese bank shares were hit hard amid SVB Financial’s fallout as fears of contagion spreading even after US authorities rushed to stem jitters about the health of its financial system. South Korea said it is closely monitoring the situation to gauge the ripple effect on its venture and startup industries. South Korean exports fall 16% y/y in first ten days of March for the five consecutive months since last October.

Thailand’s industrial sentiment in February reached its highest level in 47 months, bolstered by a rebound in domestic demand and tourism, but weak exports were a concern, an industries group said on Wednesday. The Federation of Thai Industries (FTI) said its industries sentiment index rose to 96.2 in February from 93.9 in January, marking a return to pre-pandemic levels. The tourism sector, a key driver of Southeast Asia’s second-largest economy, is expected to see 25-30 million foreign tourists this year, the government said, after beating its target in 2022 with 11.15 million visitors.

Australian jobs data stronger than expected, tempering expectations of RBA pausing as soon as next month. Australian consumer confidence held near historic lows as rising interest rates weigh heavily on sentiment and buying intentions. Similarly, Australian business confidence turned negative amid rising rates.

New Zealand GDP contracted by more than expected, strengthening views RBNZ will further step down pace of rate hikes to 25 bp in April.

FX / COMMODITIES

DXY USD index fell 0.83% to 103.70 with US Treasuries bull-steepening aggressively, as markets now imply less than a 25bp hike over the next two FOMC meetings. Data wise, Michigan sentiment came in at 63.4 (C: 67.0, P: 67.0). Retail sales mom came in in-line at -0.4% (P: 3.0%). Headline CPI came in at 0.37% mom (C: 0.4%; P: 0.51%), which brought the yoy rate down to 5.99% (C: 6.0%; P: 6.4%). However, core CPI came in a touch stronger at 0.45% mom (C: 0.4%; P: 0.4%), the largest mom increase since September. On a yoy basis, core CPI remained at 5.53% (C: 5.5%; P: 5.55%) and suggested the deceleration in inflation has stalled.

EURUSD rose 0.25% to 1.067. ECB delivered a 50bp rate hike to 3%, despite fears around financial stability, as inflation is projected to remain too high for too long. However, forward guidance is omitted as elevated uncertainty reinforces data-dependency. The rate hike is considered a dovish hike, as ECB will provide liquidity support to the euro area financial system if needed. EU final inflation February print came in in-line at 0.8%/8.5% (mom/yoy) consensus.

GBPUSD rose 1.19% to 1.2173 with broad based USD weakening. In the UK, the Spring Budget announcement was the least surprising in recent memory, as nearly all policy measures had been pre-announced. January unemployment rate fell to 3.7%, below consensus.

USDJPY fell 2.36% to 131.85 with broad based USD weakening, as US yields fell. JPY was the clear outperformer due to its safe haven characteristics and growing market participant expectations for a pause in global central bank tightening, in light of current market tensions.

Bloomberg Commodity Index fell 1.87%, as concerns over recent financial sector weakness continued. Oil led the fall, with WTI and Brent falling 12.96%% and 11.85% respectively to 82.78 and 72.97. Despite fundamental catalysts from a reopening in China, oil has been ensnared in the broader macro risk aversion stemming from recent bank liquidity concerns. In addition, IEA commented that Oil stockpiles have climbed to the highest in 18 months, with Russia managing to increase output last months despite warnings it would buckle under international sanctions. Brent crude falls to a low since December 2021. Gold and Silver rose 6.48% and 10.04% to 1989.25 and 22.602 due to broad based USD weakening, with the whole US treasuries yield curve shifted downwards.

ECONOMIC DATA

M – CH LPR, EU Trade Balance

T – NZ Trade Balance, EU Zew, CA CPI, US Existing Home Sales

W – UK CPI/PPI, US FOMC Rate Decision

Th – SZ SNB Rate Decision, NO Norges Bank Rate Decision, BOE Rate Decision, US Initial Jobless Claims/New Home Sales, EU Cons. Confid

F – JP CPI, JP/EU/UK/US Mfg/Svc/Comp PMI March Prelim, UK/CA Retail Sales, US Durable Goods Orders

Sources – Various news outlets including Bloomberg, Reuters, Financial Times, FactSet, Associated Press

Disclaimer: The law allows us to give general advice or recommendations on the buying or selling of any investment product by various means (including the publication and dissemination to you, to other persons or to members of the public, of research papers and analytical reports). We do this strictly on the understanding that:

(i) All such advice or recommendations are for general information purposes only. Views and opinions contained herein are those of Bordier & Cie. Its contents may not be reproduced or redistributed. The user will be held fully liable for any unauthorised reproduction or circulation of any document herein, which may give rise to legal proceedings.

(ii) We have not taken into account your specific investment objectives, financial situation or particular needs when formulating such advice or recommendations; and

(iii) You would seek your own advice from a financial adviser regarding the specific suitability of such advice or recommendations, before you make a commitment to purchase or invest in any investment product. All information contained herein does not constitute any investment recommendation or legal or tax advice and is provided for information purposes only.

In line with the above, whenever we provide you with resources or materials or give you access to our resources or materials, then unless we say so explicitly, you must note that we are doing this for the sole purpose of enabling you to make your own investment decisions and for which you have the sole responsibility.

© 2020 Bordier Group and/or its affiliates.