KEY MARKET MOVES

MACRO OVERVIEW

Global

Despite bank jitters and a rate hike, equities ended the week higher for a second straight week. Wagers that the Fed is done raising interest rates amid ongoing financial sector concerns helped lift sentiment.

The KBW Bank Index which posted its 3rd straight weekly decline ended Friday marginally up 0.4%. First Republic Bank continue to weigh on the index with added stress stemming from Europe’s Deutsche Bank which was under pressure from hedge funds. Over the weekend, Bloomberg reported that US authorities are considering expanding an emergency landing facility for banks in ways that would give First Republic more time to shore up its balance sheet. Officials have yet to decide what exact support is being planned but clearly the goal is to not have First Republic go down the same route as SVB and Signature Bank. Some back pedaling from Janet Yellen telling lawmakers she was prepared to take further steps to protect deposits if needed helped…a little. The Fed raised the fed funds rate by 25 bps to 5% as expected, amidst debate from its members. Atlanta President Bostic was in 2 minds to raise, Richmond President Barkin supported a ‘clear case’ for a 25 bps hike whilst St Louis’ Bullard said he expects rates to peak at a higher than expected level. Powell said at the presser that inflation has been decelerating for months but saw no potential for interest rate cuts. Eagle eyed analysts noted that in its statement, the Fed altered its wording on the future outlook to say that “some” rather than “ongoing” rate hikes are appropriate in its fight against inflation. The Fed’s dot-plot was seen as dovish given it was unchanged – the median implying one further hike remaining.

Data continue to come in mixed with the S&P Global Services PMI beating expectations whilst durable goods orders fell below expectations. A survey by the Bank of America showed investors now view a systemic credit event as the biggest tail risk to markets, followed by elevated inflation and hawkish central banks.

This week will see key data releases in GDP, personal spending and PCE Core Deflator, the Fed’s preferred inflation gauge.

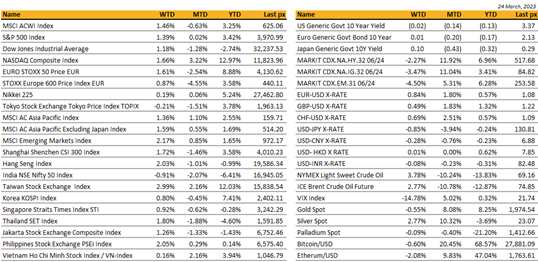

Cryptos held up well for the week with BTC pivoting around $28k and Ether circa $1800.

The not-so unloved Tech sector has continued to outperform in spite of a rate hike, banking stress and an overall neutral-at-best sentiment. Some have even referred to Tech as a safe haven. Why? It’s ‘naturally’ reacting to lower LT yields: Meta is up 71% ytd followed by Apple +23%, Alphabet +19.5%, MSFT and AMZN, both up 17% ytd. We think there Is further upside in Tech, especially in the space of generative AI.

Asia

Bank jitters and Fed took over the news headlines. Asian markets closed the week higher. MSCI Asia Pacific index was up 1.36% for the week, taking YTD gains to 2.55%. Taiwan remains the best performer YTD, up some 12% so far.

Singapore’s central bank said it will abide by the hierarchy of claims while liquidating a financial institution where shareholders will be the first to absorb losses before holders of additional Tier 1 and Tier 2 instruments. The statement comes days after bondholders were angered by Credit Suisse’s move to write down to zero 6 billion Swiss francs ($17.24 billion) of its Additional Tier 1 (AT1) debt on the orders of the Swiss regulator as part of a rescue merger with UBS. “Creditors who receive less in a resolution compared to what they would have received had the FI been liquidated would be able to claim the difference from a resolution fund that would be funded by the financial industry,” the Monetary Authority of Singapore said.

In Geopolitics, Chinese President Xi Jinping was in Russia for a three-day state visit, his first to Moscow since Russia’s invasion of Ukraine. Xi’s meeting with his neighbor and “dear friend” Vladimir Putin comes just days after the International Criminal Court issued a warrant for Putin’s arrest. Japanese Prime Minister Fumio Kishida has made a surprise visit to Kyiv, Ukraine, stealing some of the attention from President Xi. Zelenskyy called Kishida a “powerful defender of the international order” and “a longtime friend of Ukraine”. Both visits, that took place on the same day, may have been a coincidence, but it was nonetheless a signal of the growing international divide.

Japan nationwide core inflation fell back from 42-year high in-line with expectations and reflecting government’s energy subsidies. However, ex-food and energy measure hit fresh four-decade high, renewing attention on upside risks. Japan flash PMI was mixed with manufacturing contracting further to 48.6 while services expanded to 54.2, the fastest pace since 2013, underpinned by foreign travel demand.

The IMF has approved a $3B bailout to help Sri Lanka restructure its debt. The country is suffering through one of its worst-ever economic crises.

Thailand will hold a general election on May 14, with a pre-poll survey showing opposition parties holding a clear lead over military-backed establishment parties in the outgoing government led by PM Prayuth Chan-Ocha.

Tiktok– Is the platform a security risk or just another piece in the larger fight between the US and China? Allegation is that there is potential for the Chinese government to obtain the data of TikTok’s 150 million US users or influence its recommendation algorithms to push propaganda or disinformation on them. CEO Shou Zi Chew’s testimony before Congress did little to satisfy U.S. worries over TikTok’s China-based parent company ByteDance and added fresh momentum to lawmakers’ calls to ban the platform nationwide. A commerce ministry spokeswoman from China said at a news conference that China would “firmly oppose” the sale of the app. The Chinese government considers some technology — including content recommendation algorithms — to be critical to its national interest. In December last year, Chinese officials had proposed tightening the rules that govern the sale of that technology to foreign buyers. The Wall Street Journal reported U.S. authorities were considering banning TikTok ban if ByteDance doesn’t sell the company.

China has approved its first Covid-19 vaccine based on mRNA technology, greenlighting a homegrown shot months after Beijing abruptly lifted its strict pandemic restrictions. The vaccine by CSPC Pharmaceutical Group (1093.HK) was approved for emergency use by Chinese health regulator.

FX / COMMODITIES

DXY USD index fell 0.57% to 103.12 after a dovish Fed hike and market pricing in fed cuts amidst the banking turmoil which likely result in tighter credit conditions for households and businesses and to weigh on economic activity, hiring and inflation. The Fed hiked a further 25bps to put the policy rate in a target range of 4.75-5.00%, while saying in the statement that additional policy firming may be appropriate. This replaced ongoing increases in the target rate will be appropriate. So a softening in language. The pace and asset makeup of QT was unchanged as expected. The median dot plot projection showed fed funds ending 2023 at 5.1%, unchanged from December, and up by roughly one hike to 4.3% at the end of 2024. In terms of economic projections, the Fed had Core PCE inflation up modestly both this year (3.6% from 3.5% in Jan) and next (2.6% from 2.5% in Jan), but saw risks as “broadly balanced” rather than “weighted to the upside”. Data wise, March preliminary PMI all outperform consensus, manufacturing at 49.3 (C: 47.0), services at 53.8 (C: 50.3) and composite at 53.3 (C: 49.5)

EURUSD rose 0.84% to 1.076 due to broad based USD selloff. Investors priced out the chances of an imminent pause in rate hikes from the ECB. In part, that was supported by a Bloomberg article later in the session, which reported that ECB officials were growing in confidence that they had withstood the current turmoil, whilst concern remained that inflation still needed tackling. Data wise, manufacturing PMI came in lower at 47.1 (C: 49.0), but services at 54.1 (C: 52.0) and composite at 55.6 (C: 52.5) continues to outperform. Immediate support at 1.073, 1.07 and 1.067. Key psychological support at 1.05.

GBPUSD rose 0.49% to 1.2233 due to broad based USD selloff. BoE hiked 25 bps as expected to 4.25%. Looking forward, the BoE said that they still expected inflation to fall significantly in Q2, aided by falling energy prices and the government’s move to extend the Energy Price Guarantee in the budget. However, further tightening would be required if more persistent inflationary pressures. Data wise, February headline and core inflation y/y rose 10.4% and 6.2% above expectation. Retail sales m/m came in 1.2% above expectation.

USDJPY fell 0.57% to 130.73 due to broad based USD selloff. US treasury curves continued to steepen, with the short end rates falling. This reduced the US-JP yield differential. In addition, JPY was supported with risk sentiment deteriorating. Data wise, Inflation for February came in in-line at 3.3%.

Oil & Commodity- Bloomberg Commodity Index rose 0.42%, with oil prices stabilising after touching the lows since December 2011. WTI rose 3.78% to 69.26, while Brent rose 2.77% to 74.99. Gold fell 0.55% to 1978.21, after touching a high of 2010 earlier this week. Aluminium and copper rose 2.80% and 4.80% respectively, while Iron Ore fell 5.58%.

ECONOMIC DATA

M – JP PPI Svc, CH Indust. Profits, EU Money Supply, US Dallas Fed Mfg Act.

T – AU Retail Sales, US Wholesale Inv./Cons. Confid./Richmond Fed Mfg

W – SW/NO Retail Sales, UK Mortg. App, US Mortg. App/Pending Home Sales

Th – NZ Building Permits/Biz Confid., EU Cons./Econ./Indust./Svc Confid., US Initial Jobless Claims/GDP/Personal Cons./Core PCE

F – NZ Cons. Confid., JP CPI/Jobless Rate/Retail Sales/Indust. Pdtn, CH PMI, UK/CA GDP, EU Unemploy. Rate/CPI, US Personal Income/Personal Spending/Mich. Sentiment

Sources – Various news outlets including Bloomberg, Reuters, Financial Times, FactSet, Associated Press

Disclaimer: The law allows us to give general advice or recommendations on the buying or selling of any investment product by various means (including the publication and dissemination to you, to other persons or to members of the public, of research papers and analytical reports). We do this strictly on the understanding that:

(i) All such advice or recommendations are for general information purposes only. Views and opinions contained herein are those of Bordier & Cie. Its contents may not be reproduced or redistributed. The user will be held fully liable for any unauthorised reproduction or circulation of any document herein, which may give rise to legal proceedings.

(ii) We have not taken into account your specific investment objectives, financial situation or particular needs when formulating such advice or recommendations; and

(iii) You would seek your own advice from a financial adviser regarding the specific suitability of such advice or recommendations, before you make a commitment to purchase or invest in any investment product. All information contained herein does not constitute any investment recommendation or legal or tax advice and is provided for information purposes only.

In line with the above, whenever we provide you with resources or materials or give you access to our resources or materials, then unless we say so explicitly, you must note that we are doing this for the sole purpose of enabling you to make your own investment decisions and for which you have the sole responsibility.

© 2020 Bordier Group and/or its affiliates.