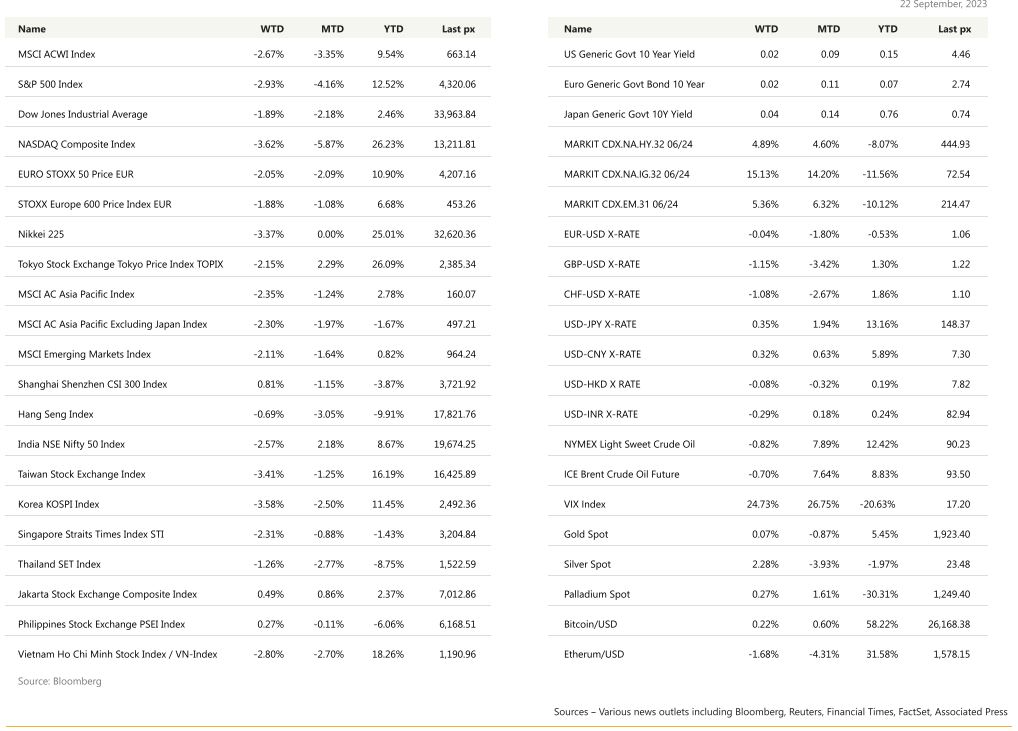

US markets endured its worst week in 6 months following the Fed’s hawkish pause statement post FOMC on Thursday. It was the weakest performance since March when fear gripped markets after the sudden collapse of Silicon Valley and Signature Banks. Tech, consumer discretionary and financials bore the brunt of the selloff. Elevated crude prices at WTI$90 pb didn’t help either. Pockets of Tech bucked the trend with Activision Blizzard Inc. shares gaining Microsoft Corp.’s $69 billion acquisition of the gaming company looked set to clear its final regulatory hurdle.

Megacaps including Nvidia Corp. and Meta Platforms Inc. rose about 1.5% and 1.1%, respectively while Broadcom fell on a report that Alphabet Inc.’s Google is considering dropping the company as a supplier for artificial intelligence chips as soon as 2027. Although the Fed left rates unchanged expectedly Thursday morning, 63% of the committee members said that they expect another rate increase by year’s end which was underscored when they increased their target rate for 2024 to 5.1% versus 4.6% previously. Rate cuts next year would only be 50 bps rather than the 100bps expected previously. However, as ex-Chair Bernanke put it previously, dot plots are but penciled-in averages and may not necessarily eventuate.

Regardless of this, higher for longer is not going away anytime soon. Treasury yield flirted with decade-plus highs with UST10’s and 2’s at 4.43% and 5.11% respectively. Outflows continued on fears of a deeper recession despite Fed’s Powell’s base case forecast that a soft landing of the US economy is still the primary objective for the FOMC.

The on-going UAW strike expanded further into the weekend against Stellantis and GM. However, the UAW announced progress in negotiations with Ford and that its strike will remain at just one facility.

Data released earlier in the week PMI data showed activity stagnated or slowed further. Applications for US unemployment benefits fell to the lowest level since January last week, and initial jobless claims dropped by 20,000 to 201,000 in the week ending Sept. 16, below expectations.

This week will see durable goods orders, annualised GDP, consumer confidence as well as the all-important PCE data Friday. Consensus is expecting core PCE Deflator MoM to come in unchanged at 0.2% and YoY at 3.9% from 4.2%.

With the VIX finally at relatively attractive ‘highs’ of 17+ we think FCN’s are compelling, in beaten down sectors we like such as commodities, given recent calls for a re-acceleration of Chinese demand and consumer staples: