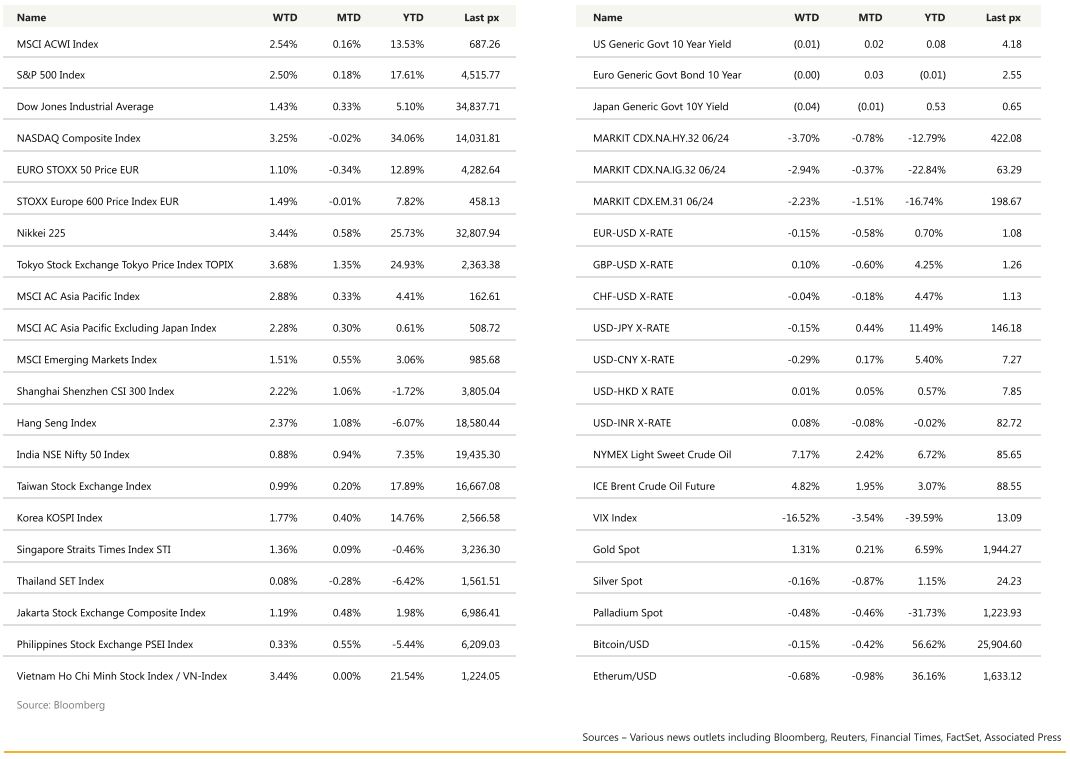

KEY MARKET MOVES

Source: Bloomberg

MACRO OVERVIEW

Global

The two key data out during the week were slightly on the disinflationary side with the PCE deflator data for July at 0.2% MoM matching expectations and Friday’s US unemployment rate ticking up to 3.8%, above expectations releasing some pressure on the Fed. On a YoY basis core PCE ex-housing deflator whilst as expected at 3.3% was above June’s 3% – a level Powell flagged as being key to bringing down to the Fed’s 2% target. NFP rose by a more than expected 187k while average hourly earnings both on a MoM and YoY basis fell in July from June providing some cooling in the labour market. Earlier in the week, we also had a glimpse into the labour market with the JOLTS release showing that job openings fell in July to a more than 2-year low, extending a gradual rebalancing in the labour market. Available positions decreased to 8.83 mln from 9.17 mln in June. Both the S&P 500 and the Nasdaq posted their first down month since February though the four-day advance between Friday and Wednesday — fuelled by a deluge of economic data and subsiding expectations of a near-term recession — narrowed the loss. In focus was oil stocks which headed for its biggest weekly gains since April (WTI$85.55, Brent $88.55) driven by a slump in US inventories and ongoing speculation that OPEC+ leaders would prolong supply cuts.

Banks also recovered from the prior week’s selloff after regulators proposed new rules around long-term debt requirements for midsized banks. Analysts described the proposal — set to impact banks with more than $100 billion in assets — as being less harsh than expected and manageable for these firms.

The VIX retreated to 13.09 despite a pick-up in UST10Y yields to 4.18%. US economic activity was revised lower with GDP at 2.1% annualised in Q2 which was below the previous estimate of 2.4%. “The market is a bit bipolar; shifting from good economic news is good for earnings, to weak economic data is good for lower inflation/ Fed being done increasing,” said one analyst, and is likely to remain so until an actual pause and/or cut eventuates.

A lighter week ahead as US markets reopen Tuesday after Monday’s Labour Day holiday. ISM and factory orders among the main releases.

A higher for longer rhetoric gives us a chance to capture these higher rates which by all accounts would probably not last that long.

We are launching a 1-year principal protected daily range accrual note at a conditional 8% pa coupon based on the following O/N SOFR ranges (terms below):

Feel free to let us know if you’d like to participate.

Asia

Asian markets are set for a positive start. Multiple Chinese lenders are set to slash deposit rates from 1-Sep, second round of cuts in less than three months. Magnitude of reductions will be larger for longer-term deposits with 3Y and 5Y rates to be cut by 25 bp while 1Y by 10 bp and 2Y by 20 bp. Move widely expected as deposit rate adjustment took cues from 10Y sovereign bond yield and 1Y LPR.

Separately, Multiple Chinese lenders are set to slash deposit rates from 1-Sep, Magnitude of reductions will be larger for longer-term deposits with 3Y and 5Y rates to be cut by 25 bp China’s largest banks have also cut interest rates on existing mortgages of CNY38.6T ($5.3T) and deposits as latest state-directed measures to revive property sector and bolster faltering economy.

The nationwide minimum down payment will also be adjusted. It will be uniformly set at 20% for first-time buyers and 30% for second-time purchasers.

Moves are part of a targeted push by authorities to shore up consumption, drive funds to equity market and alleviate pressure on banks’ margins. China’s manufacturing activity contracted for a fifth straight month in August. The official purchasing managers’ index (PMI) rose to 49.7 from 49.3 in July, still below the 50-point level demarcating contraction from expansion.

China data heat map:

Japan‘s unemployment unexpectedly rose to 2.7%. Japan’s factory output fell more than expected in July, signalling a rocky start to the second half of the year for manufacturers as worries mount over growth in China and the global economy. Industrial output fell 2% in July from the previous month, data from the Ministry of Economy , Trade and Industry showed on Thursday. The median market forecast was for a 1.4% drop. Other data showed Japanese retail sales expanded 6.8% in July from a year earlier. Median market forecast was for a 5.4% gain.

Bank of Japan board member Toyoaki Nakamura said on Thursday it was premature to tighten monetary policy as recent increases in inflation were mostly driven by higher import costs rather than wage gains.

Indonesia is introducing a golden visa scheme to attract foreign individual and corporate investors in an attempt to boost its national economy. The five-year visa requires individual investors to set up a company worth US$2.5 million, while for the 10 years visa, a US$5 million investment is required.

Forecasts for lower rainfall in September are further threatening to disrupt supplies in cereal and oilseed crops in Asia as El Nino intensifies. While wheat output forecasts are being revised lower due to dry weather in Australia, the world’s second largest exporter, record-low monsoon rains are expected to reduce the volume of crops, including rice, in India. Insufficient rains in Southeast Asia, meanwhile, could dent supplies of palm oil, the world’s most widely used vegetable oil, while extreme weather in top corn and soybean importer China is putting food output at risk.

GEOPOLITICS

Russian President Vladimir Putin will visit China to attend Belt and Road Forum in October at the invitation of President Xi. It will be Putin’s first trip overseas since ICC in the Hague announced an arrest warrant on his alleged war crimes. China is one of the places that seen could completely guarantee Putin’s security

Xi is likely to skip the G20 summit and Chinese Premier Li Qiang is expected to represent Beijing at the meeting in New Delhi, sources familiar with the matter have told Reuters.

The U.S. expanded the restriction of exports of sophisticated Nvidia (NVDA.O) and Advanced Micro Devices (AMD.O) artificial-intelligence chips beyond China to other regions including some countries in the Middle East.

Nvidia said the new licensing requirement “doesn’t affect a meaningful portion of our revenue. We are working with the U.S. government to address this matter.”

China’s Ministry of Natural Resources on Monday (Aug 28) issued the “China Standard Map Edition 2023”, which lays claims over large swathes of the South China Sea also disputed by Malaysia, Vietnam, the Philippines and Brunei, as well as several land areas in India. The map’s release comes just ahead of the Association of Southeast Asian Nations (ASEAN) grouping’s summit in Indonesia from Sept 5-7 and the Group of 20 (G20) Summit from Sept 9-10 in India, where Chinese leaders are expected to attend.

CREDIT/ TREASURIES

In the US early last week the very substantial downward revision of the July Job Opening supported risky assets even though August Conference Board Consumer Confidence printed lower than expected. 2nd Quarter GDP & Personal consumption were revised lower, GDP from 2.40% to 2.10% and personal consumption from 1.80% to 1.70%. July PCE Deflator and Core Deflator came out in line with expectations at respectively 3.30% & 4.20%, but both numbers were slightly higher than previous Month.

NFP printed slightly above expectations, but previous Month print was revised lower. Unemployment rate increased significantly from 3.50% to 3.80% but on the other hand, participation rate increase from 62.6% to 62.8%, the highest since the eve of the pandemic. August average hourly earnings MoM came out below consensus, but YoY came out in line with expectations at 4.30% but still down 0.10% compared to previous Month. However average weekly hours printed at 34.4 Vs 34.3 expected.

The impact of all these data on the US Treasury curve was some further flattening over the week. 2years yield dropped by 22bp, 5years yield dropped by 16bps, 10years yield dropped by 6bps but 30years yield was unchanged. US IG credit spread tightened by 2bps and US HY tightened by 15bps over the week. Both IG & HY gained about 0.80% last week.

FX

DXY USD rose 0.15% to 104.24 as UST yields reversed higher after the NFP. US employment report showed a further softening in the labor market. Unemployment rate rose to 3.8% (C: 3.5%). NFP came in +187k (C: 170k), but downward revisions to the prior two months. JOLTS job opening came in at 8827k in July (C: 9500k). On US other data, both 2Q23 US GDP and core PCE data were revised downwards. The price movement on US yields and USD could be explained by squaring of flattener positions or stop-outs of duration longs – and/or September is usually the beginning of a seasonally strong month for corporate bond issuance.

EURUSD fell 0.15% to 1.078. Data wise, EU CPI mom came in at 0.6% (C:0.4%), which brings the yoy estimate to 5.3% (C: 5.1%). Core CPI yoy was in-line at 5.3%. Unemployment rate was in-line at 6.4%. Final reading on Mfg for Aug came in lower than preliminary at 43.5. Technically, EURUSD closed below the 200DMA on a weekly basis, which opens the possibility of further downside. Strong support at 1.05.

GBPUSD rose 0.10% to 1.259. BoE Chief Economist said that a downturn in core inflation has not been observed, and reiterated that long term inflation expectations remain anchored, which reinforce the upward risk of further rate hikes. Data wise, Mfg August final came in at 43.0 (C: 42.5).

USDJPY fell 0.15% to 146.22, following the movement on UST yields. Short yields on the treasury curve fell for the week. USDJPY fell below 144.50 after the NFP but rebounded as UST yields rose. Technically, we see resistance level at 146.50/147.50 because of local interest to sell at these levels.

Oil & Commodity

Bloomberg Commodity Index rose 1.18% with base metals and oil rising. PBoC announced a 200-bps cut to the foreign currency reserve requirement ratio, effective September 15, pushing commodity prices higher. China also rolled out further property support measure including lower down payments for homebuyers and looser mortgage rules at major cities. WTI and Brent rose 7.17% and 4.82% respectively, closing the week at 85.55 and 88.55. Gold price rose as well, +1.31% to 1940.

ECO

Monday – JP Monetary Base, AU Inflation, SZ GDP, EU Sentix Inv. Confid.

Tuesday – AU/JP/CH/SW/EU/UK/US Svc/Comps PMI Aug Final,NZ Commodity Price, AU RBA OCR, EU PPI, US Factory Orders/ Durable Goods Order,

Wednesday – AU GDP, EU Retail Sales, US Trade Balance/ Svc/ Comps PMI Aug Final/ ISM Svc Index, CA BOC Rate Decision

Thursday – AU/CH Trade Balance, SZ Unemploy. Rate, EU GDP, CA Building Permits, US Initial Jobless Claim,

Friday – JP GDP/Trade Balance, CA Unemploy. Rate, US Wholesale Inv

Sources – Various news outlets including Bloomberg, Reuters, Financial Times, FactSet, Associated Press

Disclaimer: The law allows us to give general advice or recommendations on the buying or selling of any investment product by various means (including the publication and dissemination to you, to other persons or to members of the public, of research papers and analytical reports). We do this strictly on the understanding that:

(i) All such advice or recommendations are for general information purposes only. Views and opinions contained herein are those of Bordier & Cie. Its contents may not be reproduced or redistributed. The user will be held fully liable for any unauthorised reproduction or circulation of any document herein, which may give rise to legal proceedings.

(ii) We have not taken into account your specific investment objectives, financial situation or particular needs when formulating such advice or recommendations; and

(iii) You would seek your own advice from a financial adviser regarding the specific suitability of such advice or recommendations, before you make a commitment to purchase or invest in any investment product. All information contained herein does not constitute any investment recommendation or legal or tax advice and is provided for information purposes only.

In line with the above, whenever we provide you with resources or materials or give you access to our resources or materials, then unless we say so explicitly, you must note that we are doing this for the sole purpose of enabling you to make your own investment decisions and for which you have the sole responsibility.

© 2020 Bordier Group and/or its affiliates.