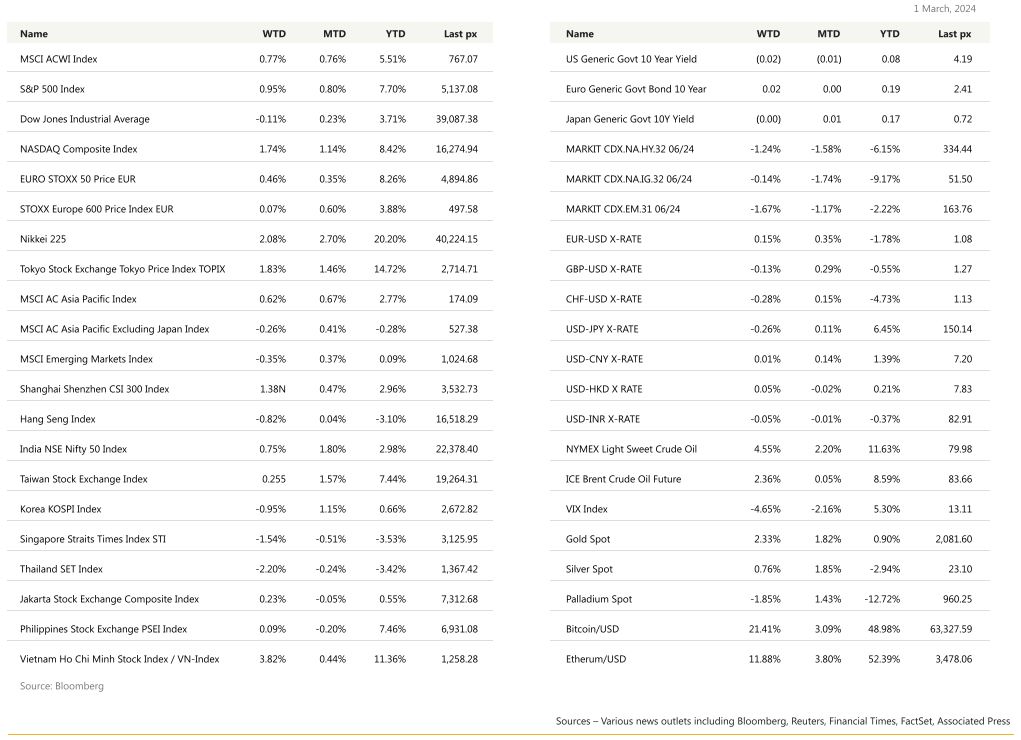

KEY MARKET MOVES

Source: Bloomberg

MACRO OVERVIEW

US

US stocks ended February with all 3 major indices notching their fourth consecutive month of gains. On the coat-tails were the mid-cap S&P 400 and small-cap Russell 2000 which also racked up consecutive monthly gains since late October last year. The S&P 500 posted muted moves for much of the week earlier, while markets awaited economic data that could provide clues to the Federal Reserve’s next moves. But following the release of the PCE core deflator, investors leaned into equities — reassured that inflation was easing enough for the central bank to eventually start cutting interest rates in the summer. Historically, February is among one of the worst months for equities, but the S&P 500 rose 5.2% for the period. The last inflation reading for the month, the PCE Index came in as expected at 2.4% which was down from last month’s 2.6%. Core came in at 2.8% from 2.9% last month. The MoM core reading came in as expected at 0.4%. The consistent easing of headline inflation, even though the pace has slowed somewhat, was enough to give risk assets the tailwind it needed to continue on its upward trajectory. Other data released underscores the economy’s continued resilience, with GDP annualised QoQ coming in at 3.2%.

February Conference Board Consumer Confidence printed much lower than expected. This data was important because it kind of validated the very weak January retail sales that were announced about two weeks ago. We will have to closely monitor the next set of data on consumption to see if a new pattern (weaker) is emerging. As a reminder, previous retail sales numbers have been very resilient, therefore one data point is not yet enough to have any real conviction about weaker consumption data moving forward. January personal income (+1.00%) was stronger than expected and previous Month (+0.40% & +0.30%) but personal spending was weaker (+0.20%).

The other closely watched by the Fed data, the U. of Mich. Inflation expectations were also on the nose at 3% and 2.9% for 1 Yr and 5-10 Yr Inflation. Fed-speak was swift on the blowers with SF’s Daly saying that they are prepared to cut rates when the data demands it. There will be 2 more inflation data (CPI & PPI) before the Fed meets again later this month.

This week’s main focus will be on jobs data, out Friday expected at NFP of 200k jobs and an unchanged unemployment rate of 3.7% as JOLTS job openings on Wednesday.

Cryptos had a spectacular showing for the week, up some 22% as the virtual community zoomed in on the impending “halving” of bitcoin. Visit www.binance.com/en/events/bitcoin-halving for more information. Gold’s rally came about following the back-on-track rate cut expectations post-PCE.

We recently added to an AI and Big Data ETF. We see Apple’s focus to AI, ditching its EV endeavours as yet another impetus for the sector to grow further. (Xtrackers AI Big Data ETF)

Europe

In the European equity markets, the STOXX 600 saw a muted performance, ending the week unchanged, while the German DAX continued its robust run, posting its seventh consecutive gain, up 1.81% for the week and reaching a new all-time high.

Regarding Eurozone data, country-level flash CPI prints for February initially caused a modest sell-off in rates. However, the figures largely aligned with expectations, showing a pattern of slowing but still above-target inflation.

German inflation reached +2.7%, French inflation was +3.1%, and Spain’s print came in slightly above expectations at +2.9%. The Euro Area-wide release later in the morning is anticipated to set the stage for the upcoming ECB meeting, with economists seeing a marginal upside risk to consensus expectations of +2.5% headline and +2.9% core inflation.

In February, the Euro Area’s Harmonized Consumer Price Index (HCIP) recorded 2.6% year-on-year (YoY) growth, while the Core HCIP registered 3.1% YoY. Additionally, the Euro Area’s Unemployment Rate fell to 6.4% in January, Economic Sentiment declined to 95.4 in February, and M3 Money Supply increased by 0.1% YoY in January.

In the UK, Food Inflation decelerated to 5.0% YoY in February, the lowest rate since May 2022, according to BRC data. CBI data indicated a moderation in the pace of Retail Sales decline, with a gauge of sales compared to a year ago rising to -7 in February. Gfk Consumer Confidence in Germany rose to -29.0 in March.

The European Central Bank (ECB) Governing Council member Kazaks warned against premature tightening, emphasizing the risks of moving too early and being compelled to hike interest rates again. ECB Vice President de Guindos outlined that monetary policy would be adjusted when inflation indicators signal an approach to the 2% target. Hawkish comments from ECB Governing Council Member Stournaras and President Lagarde, cautioning that inflation hasn’t reached the desired level, likely contributed to the market sell-off.

Asia

Asian markets were mixed last week. MSCI Asia ex Japan was lower by 0.26%. Nikkei 225 however was up almost 2.08%.

This morning, Japan’s Nikkei 225 stock index passed 40,000 points hitting a new all-time high. Japan’s consumer prices excluding fresh food rose 2% from a year ago, exceeding the consensus estimate of 1.9% and in line with the BOJ’s inflation target. The stronger-than-expected inflation data will sustain market speculation that the BOJ is nearing its first interest rate hike since 2007, a move that a majority of BOJ watchers expects to happen by April. It was the 22nd straight month in which inflation matched or exceeded the BOJ’s target.

Japan’s new births fell 5.1% in 2023 to a record-low 758,631 as the number of marriages slid 5.9% to below 500K for the first time in 90 years.

China’s manufacturing activity contracted for the fifth consecutive month, reflecting sluggish momentum as Beijing prepares to announce its annual growth target later this week. The official manufacturing purchasing managers’ index released on Friday was 49.1 for February. The non-manufacturing PMI, which covers services and construction, was 51.4 — ahead of analysts’ forecasts and up from 50.7 in January.

China is likely to maintain a gradual stimulus approach as policymakers are thought to be wary of short-term measures that entail longer-term ramifications. The NPC (National Peoples Congress) is starting tomorrow, 5th March.

The resurgence of India’s farmer protests has highlighted the Modi government’s failure to rationalise an agriculture sector that employs nearly half the population in a country where more than 800mn people rely on free, government-supplied food grains. The farmers were blocked by cement barriers and metal spikes planted on the road, while drones dropped tear gas and police fired smoke bombs and pellets, according to more than a dozen participants in the protest. They said some farmers suffered eye injuries or skin wounds. One farmer died during a clash with police at the border last week.

Singapore’s January headline and core inflation fell more than expected as 1% hike in GST was more than offset by a drop in ‘Certificate of Entitlement’ (CoE), a car ownership tax. By sector, demand-pull inflation on balance eased, giving MAS more scope to loosen policy later in 2024 Energy prices however surged 5.3% from 1.3%. Singapore’s January manufacturing production came in weaker than expected, up 1.1%.

Malaysia recorded nearly 29 million foreign arrivals last year, becoming the most popular destination in Southeast Asia, a throne that belonged to Thailand before Covid. Singaporeans were Malaysia’s biggest source of foreign arrivals with 8.3 million, followed by Indonesians, Thais, Chinese and Bruneians. Southeast Asian countries raced to attract foreign tourists with flexible immigration policies from late last year. From Dec. 1, Malaysia allowed 30-day visa-free entry for citizens from mainland China and India in a similar move to Thailand.

GeoPolitics

Israel – Hamas – US: US official says Israel has “basically signed on” to six-week ceasefire. Hamas delegation heads to Cairo for talks that could lead to temporary ceasefire, while Israel participation uncertain. US begins to airdrop food into Gaza, plans further aid missions.

Russia – US: Fresh U.S. sanctions on Moscow threaten to dent Russian oil sales to India, the biggest buyer of Russian seaborne crude, and complicate efforts by Indian state refiners to secure annual supply deals, three industry sources familiar with the matter said. Indian refiners are concerned the latest sanctions will create “challenges” in getting vessels for Russian oil and could drive up freight rates. That may narrow the discount for the oil, which is bought from traders and Russian companies on a delivered basis. An Indian government source said India would continue buying Russian oil only if it is sold below the price cap in a non-sanctioned vessels.

Credit/Treasuries

Following a string of data in the US, markets decided to focus on the weaker ISM and University of Michigan which pushed 2years Treasury yield lower over the week by 15bps, 5years lost 10bps, 10years lost 5bps & 30years lost 3bps. IG credit spreads were unchanged over the week and HY credit spreads were 5bps tighter. In term of performances, US IG gained 55bps & US HY gained 65bps. Leverage loans were marginally positive over the week.

Looking at monthly performances (for Feb) – US Treasuries posted a second straight monthly loss in the month, as yields reached their highest levels so far this year in a selloff sparked by hotter-than-expected inflation data that dented the outlook for Federal Reserve interest-rate cuts. Yields across the maturity spectrum rose to the highest levels since November or December during the last full week of the February.

Monthly yield changes for UST benchmarks: 2Y +41bp / 5Y +41bp / 10Y +34bp / 30Y +21bp.

Expectations for Fed rate cuts collapsed further, bringing them briefly in line with policymakers’ forecast from December for three quarter-point cuts this year; wagers on a March move were completely abandoned, a May cut was almost completely written off, and a June cut wound up less than fully priced in. Marketimplied inflation expectations increased during the month, aided by rising oil prices; the breakeven inflation rate for 5-year TIPS increased to 2.44% from 2.26%.

FX

DXY USD Index fell 0.07% to 103.86, as UST yields fell amidst downside US macro data and markets increase odds for June rate cut. ISM Mfg PMI falls to 47.8 (C: 49.5, P: 49.1). US Conference Board Consumer Confidence Index fell to 106.7 in February (C: 115.0; P: 110.9). US Pending Home Sales fell by 4.9% m/m in January (C: 1.5%; P: 5.7%). University of Michigan Sentiment fell to 76.9 (C: 79.6). US PCE inflation report was in line with expectations, while we have very modest downgrade to US GDP growth in Q4, with the second estimate coming in at an annualised +3.2% (vs. +3.3% first estimate).

EURUSD rose 0.15% to 1.0837. ECB Governing Council member warned against cutting rate too early. Data wise, Eurozone HCIP came in at 2.6% y/y in February (C: 2.5%; P: 2.8%) while Core came in at 3.1% y/y in February (C: 2.9%; P: 3.3%). Unemployment Rate fell to 6.4% in January (C: 6.4%; P: 6.5%). Economic Sentiment fell to 95.4 in February (C: 96.6; P: 96.1). Support at 1.08/1.075, resistance at 1.087/1.095.

GBPUSD fell 0.13% to 1.2655, despite weaker USD and positive risk sentiment. Data wise, UK Mortgage approvals came in at 55.2k (C: 52.0k, P 50.5k), while final Mfg PMI came in higher at 47.5. Resistance at 1.27/1.275, support at 1.26/1.254.

USDJPY fell 0.26% to 150.12, driven by weaker USD and lower UST yields. BoJ Governor Ueda says he does not believe the 2% price target is in sight and that he will closely monitor wage growth developments last friday, a different view than BoJ Board Member Takata. Data wise, Japan inflation slowed less than expected in Jan, rising 2.2% yoy (C: 1.9%, P: 2.6%), while core at 2.0% (C: 1.9%, P: 2.3%) and core-core at 3.5% (C: 3.3%, P3.7%). Retail sales mom at 0.8% (C: 0.5%, P: -2.9%), yoy at 2.3% (C: 2.0%, 2.1%). Immediate resistance at 150.80/151.50, support at 150/149.20.

Oil & Commodities

Crude Oil gained last Friday, with WTI and Brent rising 4.55% and 2.36% to close at 79.97 and 83.55 respectively, driven by positive risk sentiment, as markets increase odds for a June rate cut. The US Energy Information Administration said oil demand touched a four-year high in 2023 and would likely hold near that level this year.

Gold rose 2.33% to 2082.92 (new ytd weekly high), with more than USD 30 gain last Friday after the weak USM mfg, driven by weaker USD and lower UST yields. 2 years yield fell more than 15 bps.

Economic News This Week

-

Monday – JP Capital Spending, AU Melbourne Inflation/ Building App., SZ CPI, EU Sentix Inv. Confid.

-

Tuesday – AU/JP/CH/EU/UK/US Svc/Comps PMI Feb Final, JP Tokyo CPI, NZ ANZ Commod. Price, EU PPI, US Factory Orders/ISM Svc/Durable Goods

-

Wednesday – AU GDP, UK Construc. PMI, EU Retail Sales, US MBA Mortg. App/ADP Employ./JOLTS, CA BOC Rate Decision

-

Thursday – AU Trade Balance, CH Trade Balance, SZ Unemploy. Rate, EU ECB Deposit Rate, US Trade Balance/ Initial Jobless Claims

-

Friday – JP Current Acc, EU GDP, CA Unemploy. Rate, US NFP/Unemploy. Rate

Sources – Various news outlets including Bloomberg, Reuters, Financial Times, FactSet, Associated Press

Disclaimer: The law allows us to give general advice or recommendations on the buying or selling of any investment product by various means (including the publication and dissemination to you, to other persons or to members of the public, of research papers and analytical reports). We do this strictly on the understanding that:

(i) All such advice or recommendations are for general information purposes only. Views and opinions contained herein are those of Bordier & Cie. Its contents may not be reproduced or redistributed. The user will be held fully liable for any unauthorised reproduction or circulation of any document herein, which may give rise to legal proceedings.

(ii) We have not taken into account your specific investment objectives, financial situation or particular needs when formulating such advice or recommendations; and

(iii) You would seek your own advice from a financial adviser regarding the specific suitability of such advice or recommendations, before you make a commitment to purchase or invest in any investment product. All information contained herein does not constitute any investment recommendation or legal or tax advice and is provided for information purposes only.

In line with the above, whenever we provide you with resources or materials or give you access to our resources or materials, then unless we say so explicitly, you must note that we are doing this for the sole purpose of enabling you to make your own investment decisions and for which you have the sole responsibility.

© 2020 Bordier Group and/or its affiliates.