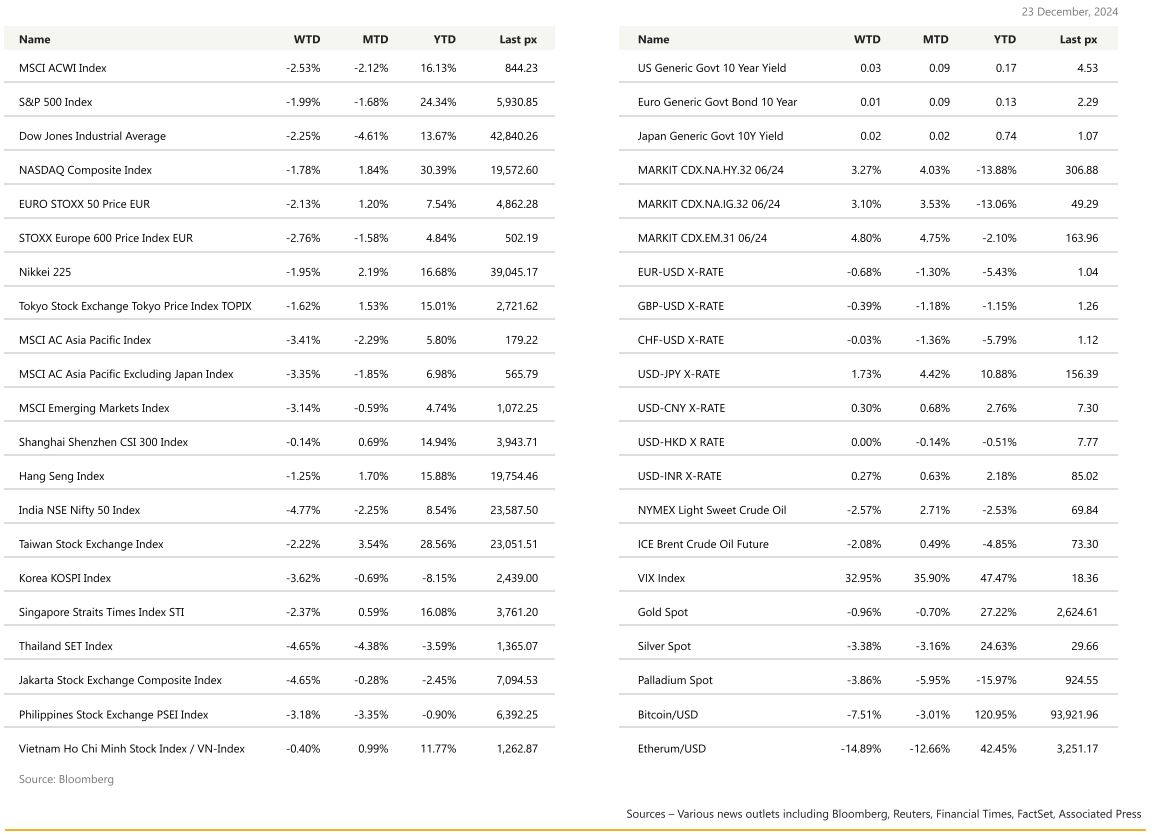

KEY MARKET MOVES

Source: Bloomberg

MACRO OVERVIEW

US

US stocks staged a rebound on Friday, but it wasn’t enough to stem the week’s retreat which saw the S&P 500 close down 1.97% for the last full trading week of the year. Concerns surrounding the Trump Administration’s new policies being inflationary and a resilient economy prompting the Fed to revise its dot plot, dampened sentiment. The Fed lowered interest rates as expected by 25 bps to 4.25% – 4.50%. Jerome Powell jolted US stocks as hawkish projections from the Federal Reserve sparked the biggest rout since early August, with the indices falling 3% in one session. The Fed chief sharply changed his focus back toward fighting inflation from supporting what had been a weakening labour market.

But aside from the decision itself, just about every other aspect leant in a more hawkish direction than expected. For instance, the latest dot plot only penciled in 50bps of cuts for 2025, down from 100bps in September and less than the 75bps expected by consensus. Similarly, the long-run median dot moved up to 3.0%, whilst the inflation projections saw a visible upgrade, with 2025 PCE inflation now seen at 2.5% (vs. 2.1% before). Indeed, most FOMC members now see the risks to core PCE as tilted to the upside, and Cleveland Fed President Hammack voted against the rate cut altogether. Finally, the Fed also predicted that unemployment rate would steady at 4.30%.

That hawkish tone was followed up by Chair Powell in the press conference, who said that the latest rate cut “was a closer call”, and they were “at a point at which it would be appropriate to slow the pace of rate cuts”. Powell repeatedly noted that they need to see more “progress on inflation” to cut rates further, and said they were “not going to settle” for inflation staying above 2%. Some US economists see the meeting as reinforcing their baseline view that a skip at the January meeting will likely turn into an extended pause in 2025. The market is now expecting more skips at next year’s meetings!

Europe

The European Stoxx 600 index closed -2.76% lower for the week with almost all sectors in negative territory.

In terms of data, the Euro area composite output PMI increased 1.2pts to 49.5. This came as a relief after the 1.8pts decline seen the prior month. The manufacturing sector remains very weak, with the manufacturing output reading flat at 45.2 and we saw a significant rebound in services to 51.4. At the country level, the composite output reading increased 0.6pt to 47.8 in Germany. It increased 0.7pt in France. Consumer confidence in the Euro area declined by 0.7% to -14.5%. This is the second consecutive decline and provides further signs that consumers have turned more pessimistic into year end. The November final Eurostat Euro area inflation print was broadly in line with the flash estimate. Headline inflation was revised down 0.1pp to 2.2% y/y in the final November release, while core was unrevised at 2.7% y/y.

All in all, this week’s data, along with other hard and soft indicators collected so far, paint a picture of weak activity momentum at the end of Q4. The labor market continues to cool, the manufacturing sector shows no signs of turnaround, and growth in the services sector is likely to remain sluggish in the short run.

Over in the UK, The Bank of England (BoE) opted to keep its key interest rate unchanged at 4.75% on Thursday, as widely expected. The Monetary Policy Committee (MPC) voted 6-3 in favor of holding rates, with three members dissenting and advocating for a 25bps cut to 4.5%, indicating growing dovish sentiment within the committee amid mounting economic concerns. The MPC gave a relatively strong signal that its previous baseline of a gradual easing of 100bp was intact.

The statement was mixed and saw elements of both arguments represented. While the statement partially dismisses some of the recent wage strength as volatility, there was a recognition that inflation expectations had moved higher of late. Traders interpreted the BoE’s decision as a dovish hold, prompting a shift in money markets. The GBP Overnight Index Swap (OIS) curve – which reflects market-based expectations over the Bank Rate in the future – now suggests a 72% likelihood of a rate cut at the February meeting, up from 55% before the decision. Markets are pricing in 22bps of easing by the end of first quarter 2025, with expectations of two 25bps cuts over the course of next year. Yields on rate-sensitive 2-year gilts fell by 4 basis points, reflecting increased expectations for imminent rate cuts. Meanwhile, the 10-year gilt yield slipped below 4.6%.

The British pound weakened slightly, sliding from $1.2650 to $1.2600 after the announcement, trimming earlier daily gains from 0.7% to 0.2%. In equities, the FTSE 100 rebounded by 0.4%, benefitting from expectations of looser monetary policy.

In terms of data, headline CPI inflation for November rose from 2.35 to 2.6%. Core inflation was up from 3.3% to 3.5%. Services inflation held at 5.0%.

Data over the Christmas and new year period is light but we will see the final Q3 GDP this week in the Euro area today.

Asia

Markets in Asia closed the week lower. MSCI Asia was down 3.4%, Nikkei was lower by 1.95%. India was the worst performer, lower by 4.77% for the week. Taiwan is on track to being the best performing market YTD, already up 28.56% for the year.

China’s retail sales growth for November disappointed, increasing only 3% year-on-year, below forecasts. Industrial production grew 5.4% year-on-year, aligning with expectations, but fixed asset investment slowed as property investment declines deepened. House price declines in major cities moderated, while industrial production growth indicated a manufacturing recovery. Credit data released late Friday showed weaker-than-expected new loans. Chinese banks left LPRs unchanged as widely expected with 1-year at 3.10% and 5-year at 3.60%. Attention shifts to a possible 25 to 50 bp RRR cut by end-year to free up CNY500B to 1T of funds, taking into account liquidity arrangements for Lunar New Year.

Japan’s manufacturing activity contracted for the sixth consecutive month in December, though at a slower pace. Machinery orders rebounded in October, and exports rose 3.8% year-on-year in November, exceeding expectations due to a weaker yen and robust global demand. Bank of Japan Governor Kazuo Ueda suggested more time was needed to assess wage growth and global market impacts before deciding on an interest rate rise, leading to a yen depreciation. The next BoJ meeting is scheduled for January 23-24. South Korea’s finance minister noted reduced uncertainties following Yoon’s impeachment, highlighting the country’s strong economic system. The Bank of Korea pledged to use all available tools to manage volatility in financial and foreign exchange markets.

Other data points from Asia: India’s composite PMI surged to a four-month high in December, driven by growth in both the manufacturing and service sectors. Singapore’s home sales in November reached their highest level in a decade, signalling robust demand in the property market. Bank Indonesia maintained its 7-day reverse repo rate at 6.0%, focusing on stabilizing the rupiah amid global uncertainties. The Bank of Thailand kept its 1-day repo rate unchanged after last month’s unexpected 25-basis-point cut. GDP growth showed improvement, supported by fiscal spending and consumer stimulus, while inflation, at around 1% in November, remained below the central bank’s 1-3% target range. Vietnam’s exports grew by 8.2% year-on-year (YoY) in Nov, as key export categories continued to show robust growth. Malaysia’s headline CPI inflation edged down to 1.8% in Nov (vs. 1.9% in Oct) mainly driven by slower communication service inflation. Philippines central bank decided to cut interest rate by 25bps despite the US hawkish signals, which is the third rate cut by the country this year.

GeoPolitics

Russia – Ukraine: After nearly three years of conflict, the war in Ukraine appears to be nearing an endgame. Ukrainian President Volodymyr Zelenskyy has shown openness to diplomatic solutions, signalling willingness to accept a ceasefire without the immediate return of all territories seized by Russia since 2014. But he has warned that security guarantees solely from European countries, without US involvement, will not be “sufficient” to ensure the long-term protection of Ukraine from any further Russian aggression. Russian President Vladimir Putin has expressed readiness for talks, including potential discussions with U.S. President-elect Donald Trump, without preconditions. Meanwhile, Ukraine’s security service (SBU) assassinated a senior Russian general responsible for nuclear, biological, and chemical protection forces, accusing him of involvement in chemical weapon use.

Israel – Syria: HTS leader Mohammed al-Golani has condemned Israel’s airstrikes on ousted dictator Assad’s military assets, but says his priority is rebuilding a more united Syria rather than getting drawn into regional disputes. Ditto, Israeli leader Benjamin Netanyahu says he has no interest in a conflict with Syria, though he just announced plans to double the Israeli population in the Golan Heights (widely recognised as Syrian territory). Meanwhile, Israel has decided to close its embassy in Ireland citing “anti-Israel policies”.

China – India: China expressed readiness to stabilize bilateral relations with India through high-level talks, emphasizing mutual trust, dialogue, and the peaceful resolution of border issues. India also acknowledged the discussions aimed at maintaining peace and exploring solutions to longstanding boundary disputes.

China – US: China accused a U.S. intelligence agency of cyberattacks targeting its advanced materials and high-tech sectors, though it did not specify which agency. Additionally, the U.S. Department of Defence reported a 20% expansion of China’s People’s Liberation Army arsenal in 2023, projecting 1,000 operational warheads by 2030, as global attention shifts to President-elect Trump’s approach to China and Taiwan.

China defence: People’s Liberation Army continues a rapid expansion according to the US defence department. The Pentagon said the PLA had expanded its arsenal by 20 per cent in the 12 months from mid-2023 and was on track to have 1,000 operational warheads by 2030. The report, which is mandated by Congress, comes as president-elect Donald Trump prepares to take office in January. Defence experts are waiting to see what approach he will take on China and Taiwan.

US- Pakistan: A senior White House official said last week that the nuclear-armed Pakistan is developing long-range ballistic missile capabilities that eventually could allow it to strike targets well beyond South Asia, making it an “emerging threat” to the United States.

US- Panama: President-elect Donald Trump threatened to reassert U.S. control over the Panama Canal on Sunday, accusing Panama of charging excessive rates to use the Central American passage and drawing a sharp rebuke from Panamanian President Jose Raul Mulino. Trump also said he would not let the canal fall into the “wrong hands,” warning of potential Chinese influence on the passage.

Credit Treasuries

The US Treasury curve bear steepened after the December FOMC with the 2years yield up 8bps, 5, 10 & 30years yield gained 15bps, the 10years yield closing the week >4.53%, its highest level since May 2024. US 5years IG credit spread widened by 2bps while US HY credit spread widened by 11bps. In term of performances, US IG lost 1.40% over the week, US HY lost 0.70% and US leverage loans lost 20bps.

Ten-year CGB yield slumped to fresh low at 1.71% on Monday as China’s bond rally continued as strong of weak economic data boosted demand for haven assets. Citi’s economists said lower yields may persist into next year as PBOC pledged more accommodative monetary policy

FX

DXY USD Index rose 0.58% to close the week at 107.62, driven by the hawkish cut by the Fed. The Fed delivered a widely expected 25 bps cut, taking the fed funds rate down to the 4.25-4.50% range. However, the latest dot plot only pencilled in 50bps of cuts for 2025, down from 100bps in September and less than the 75bps expected by consensus. Similarly, the long-run median dot moved up to 3.0%, whilst the inflation projections saw a visible upgrade, with 2025 PCE inflation now seen at 2.5% (vs. 2.1% before). Most FOMC members now see the risks to core PCE as tilted to the upside. In addition, Chair Powell repeatedly noted that they need to see more “progress on inflation” to cut rates further, and said they were “not going to settle” for inflation staying above 2%.

European Currencies fell against USD, with EURUSD -0.68% to 1.043 and GBPUSD -0.39% to 1.257. Eurozone macro data was mixed, manufacturing PMI in line, steady at 45.2 in December, consensus at 45.3. Services beat, up 1.9pts to 51.4, consensus looked for no change. Final print for Eurozone CPI revised down slightly, now at 2.2%yoy for November, previously 2.3%. Core unchanged at 2.7%yoy. German Chancellor Scholz lost a vote of confidence as expected, paving the way for an election on 23 February, adding to EUR weakness. BoE kept rates on hold at 4.75% as expected, but with a 6-3 vote with the minority preferring a 25bp cut. The statement made clear that the path was still towards further easing, and that a “gradual approach to removing monetary policy restraint remained appropriate.” UK macro data was mixed, UK manufacturing PMI missed, down 0.7pts to 47.3 in December, consensus looked for a 0.5pt gain. Services beat, up 0.6pts to 51.4, consensus looked for a 0.2pt gain. Strong beat on UK employment, up 173k in 3mths to October, consensus at +5k. Unemployment steady at 4.3%, in line with consensus. Wages beat, up 5.2%yoy, consensus at 4.6%.

Antipodean Currencies fell significantly against USD, with AUDUSD -1.74% to 0.6251 and NZDUSD -1.94% to 0.5652, aggravated by negative risk sentiment. NZ GDP fell 1% qoq in Q3, prior quarter also revised lower, leaving growth at -1.5% over the year. Economy is in deep recession, and with 125bps of easing already delivered

USDJPY rose 1.73% to close the week at 156.31. BoJ kept rates unchanged at 0.25% as expected. However, the statement from BoJ and press conference from Governor Ueda both leaned dovish. The statement stated the high uncertainties surrounding Japan’s economic activity and prices, whereas Governor Ueda wants more clarity from wages and President Trump’s policy before proceeding with the rate hike. Data wise, headline CPI moved back up to +2.9% in November as expected, whilst corecore inflation was up to a 7-month high of +2.4%.

USDCAD rose 0.88% to close the week at 1.4359, at one point reaching a year to date high of 1.4467, as Prime Minister Justin Trudeau’s government slips into crisis after the shocking resignation of his finance minister, with politics driving CAD weakness. Data wise, Canada CPI missed at headline but core stronger. Headline up 1.9%yoy in November, consensus at 2%; trimmed mean at 2.7%yoy, consensus at 2.6%, but month-onmonth in line, beat reflects upward revision to month prior.

Scandinavian Currencies fell against USD, with USDNOK +1.59% to 11.3206 and USDSEK +0.46% to 11.0283. Riksbank cut by 25bps to 2.5%, as expected. However, details lean hawkish, with rate path for Q1 implying 50% chance of a further rate cut in January, against market that is fully priced. Norges bank kept policy on hold at 4.5%, as expected. Guidance points to 50bps of cuts in 2025, a further 60bps in 2026.

Oil & Commodities

Oil Futures fell last week, with WTI falling 2.57% to 69.46 and Brent falling 2.08% to 72.94, driven by hawkish Fed rhetoric on rate cuts guidance. Gold fell 0.96% to 2622.91, driven by rise in Treasury yields and USD. With RSI below 50, downward trend is still intact. Strong support level at 2570/2540.

Economic News This Week

-

Monday – UK GDP, CA GDP, US Building Permits/Durable Goods Orders/New Home Sales/Cons. Confid.

-

Tuesday – AU RBA Minutes, US Richmond Fed Mfg

-

Wednesday – JP Machine Tool Orders

-

Thursday – US Initial Jobless Claims

-

Friday – JP Tokyo CPI/Indust. Pdtn, US Wholesale Inv.

Sources – Various news outlets including Bloomberg, Reuters, Financial Times, FactSet, Associated Press

Disclaimer: The law allows us to give general advice or recommendations on the buying or selling of any investment product by various means (including the publication and dissemination to you, to other persons or to members of the public, of research papers and analytical reports). We do this strictly on the understanding that:

(i) All such advice or recommendations are for general information purposes only. Views and opinions contained herein are those of Bordier & Cie. Its contents may not be reproduced or redistributed. The user will be held fully liable for any unauthorised reproduction or circulation of any document herein, which may give rise to legal proceedings.

(ii) We have not taken into account your specific investment objectives, financial situation or particular needs when formulating such advice or recommendations; and

(iii) You would seek your own advice from a financial adviser regarding the specific suitability of such advice or recommendations, before you make a commitment to purchase or invest in any investment product. All information contained herein does not constitute any investment recommendation or legal or tax advice and is provided for information purposes only.

In line with the above, whenever we provide you with resources or materials or give you access to our resources or materials, then unless we say so explicitly, you must note that we are doing this for the sole purpose of enabling you to make your own investment decisions and for which you have the sole responsibility.

© 2020 Bordier Group and/or its affiliates.