/ Monthly Market Update - May 2026

The Slow Erosion of the Petrodollar

For half a century, oil helped anchor the dollar at the centre of the global system. Today, that anchor is loosening, giving way to a more plural and less predictable monetary order.

Table of Contents

Insights

From Monetary Hegemony to Monetary Optionality

For much of the past half century, the dominance of the US dollar has rested on more than economic size or financial depth. It has been reinforced by a dense web of trade relationships, security guarantees, and the central role of energy markets. At the heart of this system sat the petrodollar: the convention that oil, the world’s most strategically important commodity, is priced and settled in US dollars, with surplus revenues recycled into dollar assets – namely the US treasuries.

Today, that architecture is under growing strain. The erosion of the petrodollar does not point towards the immediate collapse of dollar dominance, nor its replacement by a rival currency. Instead, it signals a gradual transition from monetary hegemony to monetary optionality—a world in which the dollar remains central but less exclusive, and where trade, finance, and reserves become more fragmented across currencies and assets.

In this article, we argue that the adjustment is being driven by three interlinked forces: the geographic re orientation of energy demand towards Asia; a slow but consequential shift away from globally traded fossil fuels; and the re emergence of gold as a neutral reserve asset in a more contested geopolitical landscape. Understanding how these forces interact is essential for long term portfolio construction.

What Is the Petrodollar and How It Was Sustained

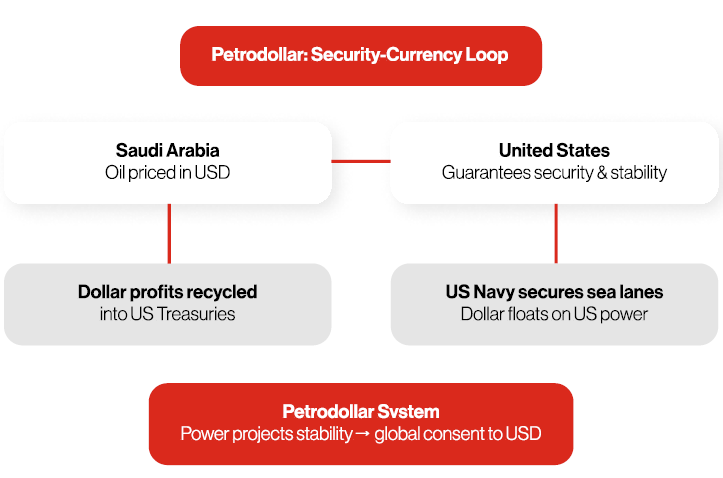

The modern petrodollar system emerged in the aftermath of the collapse of Bretton Woods. In the early 1970s, as the dollar severed its link to gold, the United States reached a strategic understanding with Saudi Arabia and, by extension, the wider Gulf. Oil would be priced and settled in US dollars; energy exporters would invest their growing surpluses in dollar assets, particularly US Treasuries; and the United States would provide security guarantees for key producers and shipping routes (as seen in Figure 1).

This arrangement proved remarkably durable. Oil’s centrality to global manufacturing, transport, and agriculture meant that dollar pricing created a powerful incentive for corporates and sovereigns alike to operate in dollars. Trade invoicing, banking systems, and reserve accumulation followed naturally. Energy exporters recycled their surpluses into US financial markets, lowering funding costs for the US and deepening the liquidity of dollar assets. The dollar’s role as the world’s reserve currency was not merely a monetary outcome, but the by product of a tightly integrated geopolitical and economic/trading system.

Figure 1: Security-Currency Loop

The Geography Shift — Oil Demand Has Moved, the Monetary System Has Not

The first structural fault line in the petrodollar system lies in the geography of energy demand. Over the past two decades, the centre of gravity of global oil consumption has shifted decisively away from the United States and Europe towards Asia. China, India, and other emerging Asian economies now account for the bulk of incremental demand, while the United States—once the lynchpin consumer of Middle Eastern oil—has moved close to energy self‑sufficiency.

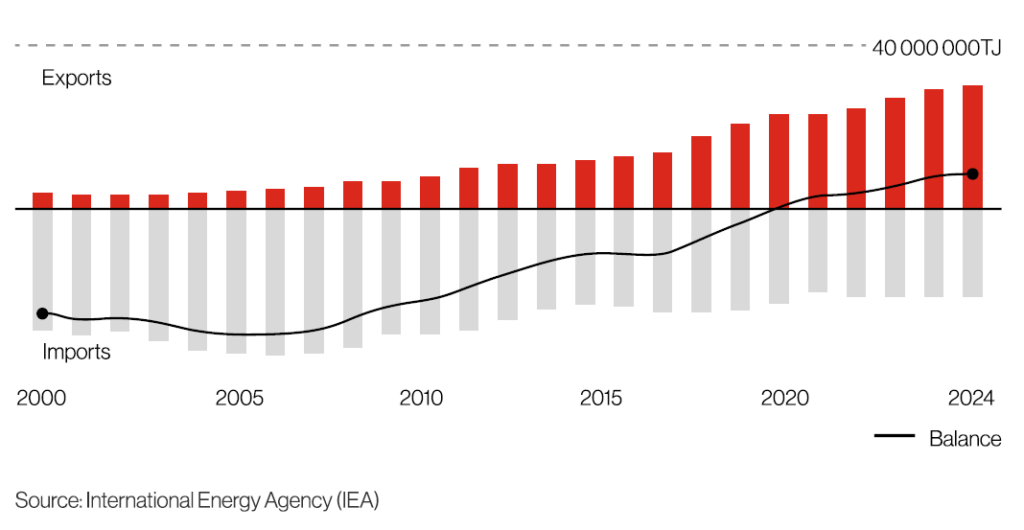

Figure 2: US becomes net Exporter of energy since 2019

This shift was reinforced by changes on the supply side. The US shale revolution marked a decisive inflection point, transforming the United States from the world’s largest oil importer into a major producer and, increasingly, a net exporter (Figure 2). In doing so, it weakened the economic symmetry that had long underpinned the petrodollar arrangement.

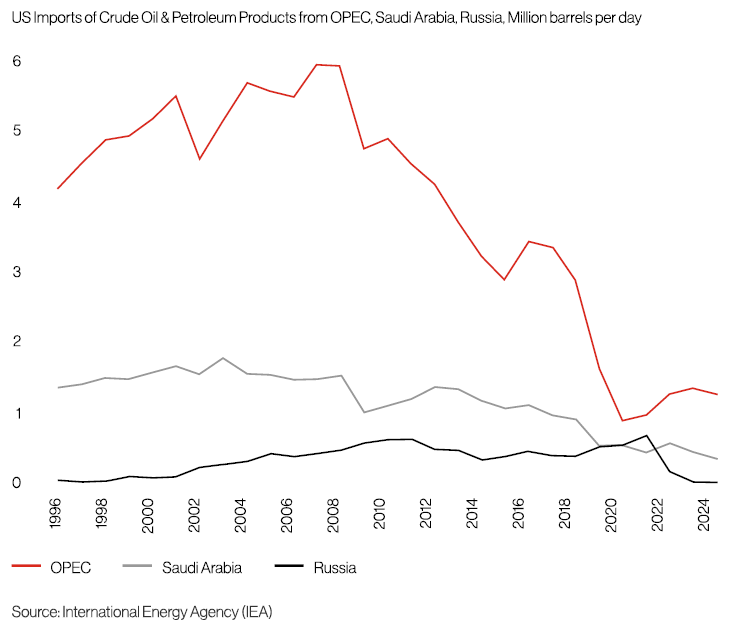

Energy independence reduced Washington’s direct reliance on Gulf supply (Figure 3), while expanding US output began to compete with OPEC exports in global markets, particularly in Europe and Asia. As dependence gave way to optionality, the implicit linkage between Gulf oil production and unconditional US security guarantees became less automatic and thus laying the groundwork for a more fragmented monetary and geopolitical order.

Figure 3: US imports of Crude and Petroleum from Middle East and other oil producing nations drop

Yet while energy flows and strategic incentives have evolved, the monetary architecture of oil markets has been slower to adjust. Oil invoicing and settlement remain overwhelmingly dollar‑centric, even though most Middle Eastern crude now flows east rather than west. This growing misalignment introduces increasing friction. For Asian importers, settling energy trade in dollars entails higher funding costs, currency mismatches, and reliance on dollar liquidity at a time when trade relationships, capital flows, and political alignments are becoming more regionalised.

Against this backdrop, the growing interest among Asian buyers, and some producers, in non‑dollar settlement reflects pragmatism rather than provocation. It is less a statement of geopolitical intent than a recognition that the assumptions underpinning the petrodollar—US‑centric trade flows supported by unchallenged security guarantees—no longer fully reflect the structure of the global economy. The result is a widening gap between where energy is consumed, how it is financed, and which currency system best serves those realities.

Energy Transition as a Currency Event (in Slow Motion)

A second, more gradual force reshaping the petrodollar sits beneath the daily focus on oil pricing and settlement: the steady reconfiguration of the global energy mix itself. While attention often centres on alternative currencies and payment systems, a deeper shift is underway as oil’s share of primary energy consumption begins to decline across a growing number of economies. This transition is uneven and protracted, but its monetary implications are no less consequential for being slow.

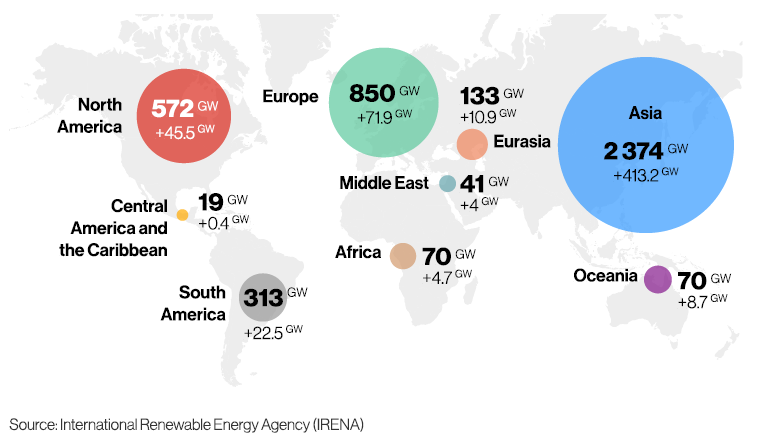

The experience of repeated energy shocks over the past decade has reinforced the strategic imperative for countries to reduce reliance on imported fossil fuels. Yet the response has diverged sharply by region (Figure 4). The United States has prioritised energy resilience through domestic oil and gas production, while China and large parts of the Global South and Europe have accelerated investment in electrification via renewable power generation. The objective is increasingly clear: to electrify as much economic activity as possible and maximise carbon‑free electricity supply, thereby reducing exposure to volatile commodity markets and external supply risks.

Figure 4: Renewable power additions vary by regions

China’s role in this transition is particularly significant. Through sustained industrial investment, it has established dominance across key decarbonisation technologies, including electric vehicles, solar photovoltaics and battery storage. As a result, China is not merely reducing its own dependence on imported hydrocarbons but positioning itself as the central supplier of the technologies that will underpin the next energy system.

None of this suggests that the world will trade materially fewer barrels of oil across borders in the foreseeable future. Oil remains deeply embedded in industrial processes, transport, and military logistics, and there is little evidence that global peak consumption is imminent in the short term.

Rather, the more relevant shift lies in oil’s relative importance. As the share of oil in global energy demand gradually declines in favour of electrification and low‑carbon power, the monetary infrastructure built around energy trade becomes incrementally less central. The consequence is not a sudden break in dollar demand, but a slow erosion of the structural forces that once made energy markets a uniquely powerful pillar of dollar dominance.

The Security Layer — When the Dollar’s Anchor Is Tested, Dominance Gives Way to Fragmentation

The petrodollar was never purely a market convention. It was anchored by security. The credibility of US guarantees—from physical protection of Gulf producers to maritime security in strategic chokepoints—underpinned confidence in the dollar’s role in energy markets.

Today, that security layer is more contested. Geopolitical tensions in the Middle East, the weaponisation of trade routes, and the selective enforcement of sanctions have sharpened awareness of vulnerability. Even traditional allies are reassessing the depth and permanence of US security commitments, while the United States itself is increasingly selective in its global engagements.

This does not imply a sudden withdrawal, but it does mark a shift from dominance to fragmentation. As security guarantees become more conditional, countries seek greater autonomy across energy, defence, and finance. Currency decisions increasingly reflect this logic. The result is a more plural monetary environment, where reliance on a single issuer or settlement system is seen not as efficiency, but as concentration risk.

The Return of History — Why Diversification Flows to Gold, Not Fiat

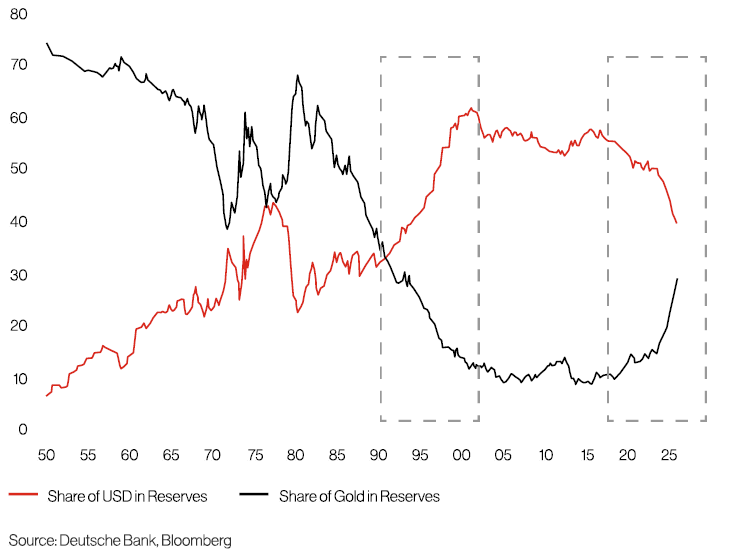

One of the most striking features of recent reserve diversification is where it has not gone. The decline in the dollar’s share of global reserves (Figure 5) has not been matched by a commensurate rise in other fiat currencies. Instead, gold has absorbed the bulk of marginal diversification.

This reflects the broader “return of history” in global finance. The post Cold War period saw declining geopolitical risk, expanding global trade, and rising confidence in fiat monetary systems. In that environment, gold’s role faded. Today’s conditions are different. Sanctions regimes, geopolitical rivalry, higher fiscal risk, and concerns over the accessibility of foreign savings have returned to the fore.

Gold’s appeal lies in its neutrality. It is no one’s liability, cannot be frozen by a foreign authority, and sits outside payment systems. For emerging market reserve managers, it provides insurance against both financial and political risk. The resurgence of gold is not a nostalgia trade; it is a rational response to a more contested international order.

From Petrodollar to Reserve Stack: How Energy, FX, and Gold Interlock

Viewed together, these developments point to an evolving reserve “stack”. Energy trade determines settlement needs; settlement currencies shape reserve accumulation; and reserves reflect assessments of security, liquidity, and political risk.

As oil trade becomes more regional and less central to global growth, demand for dollar settlement grows more discretionary. At the same time, the incentive to hold large pools of dollar reserves weakens, particularly when those reserves may be politically vulnerable.

Gold increasingly fills the gap—not as a replacement for the dollar, but as a complement in a more diversified reserve framework. Gold serves as a form of geopolitical insurance. Treasury holdings and access to SWIFT can be frozen at any time. It’s more challenging to do the same with physical gold stored in a domestic vault.

This layered system marks a departure from the simplicity of the petrodollar era. Monetary power becomes more diffused, and currency dominance is measured less by exclusivity than by continued relevance.

Portfolio Construction Implications — Positioning for Regime Drift

For investors, the implications are subtle but significant. This is not a setup for abrupt de‑dollarisation trades or wholesale regime collapse. Rather, it argues for portfolios designed to navigate regime drift.

In foreign exchange, the likely outcome is greater dispersion rather than a single directional move. The dollar remains dominant, but currency volatility rises as trade patterns fragment. In reserves and real assets, gold regains strategic relevance—not merely as an inflation hedge, but as a monetary asset reflecting geopolitical optionality.

In rates and sovereign debt, reduced automatic recycling of surpluses into US Treasuries implies greater sensitivity to fiscal dynamics and term premia. Energy exposure, meanwhile, increasingly reflects balance‑of‑payments dynamics and strategic resilience rather than pure cyclical demand.

Several variables could alter the pace or direction of this transition. A renewed expansion of global trade, credible reinforcement of multilateral security guarantees, or a sustained increase in emerging market reserve accumulation could stabilise the existing system. Conversely, escalation of geopolitical conflict, deeper fragmentation of energy markets, or further weaponisation of finance could accelerate diversification away from dollar‑centric frameworks.

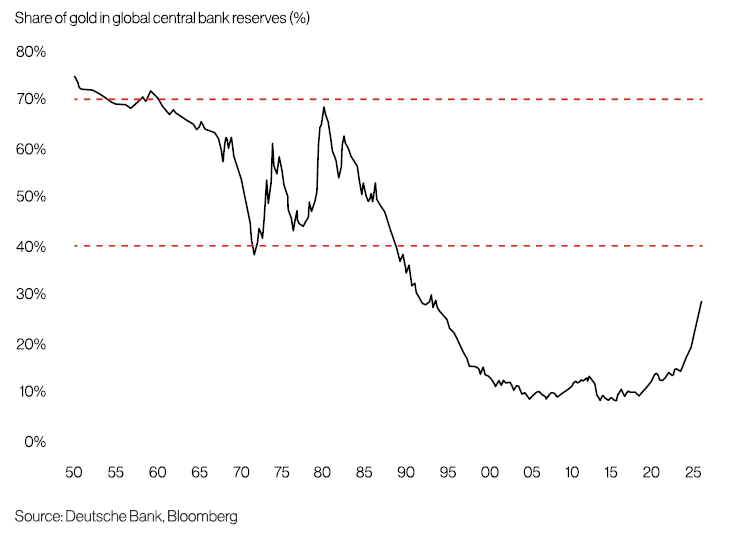

The adjustment is not linear. It will be shaped by policy choices, shocks, and strategic responses that are difficult to model but important to monitor. But the trajectory looks clear as share of Gold in Global central banks inch towards long term average levels (Figure 6).

The End of the Petrodollar Is Not the End of the Dollar

The petrodollar was a powerful mechanism for embedding trust in a US‑led economic and security order. That order is evolving. As energy demand shifts, trade fragments, and security becomes more conditional, the logic of exclusive dollar dominance weakens. Yet the dollar’s depth, liquidity, and institutional backing ensure its continued centrality.

What is changing is not the dollar’s relevance, but its monopoly. The world is moving towards monetary optionality—where currencies, assets, and systems coexist rather than dominate. In that world, gold’s resurgence and the petrodollar’s erosion are not contradictions, but reflections of the same underlying transition. For investors, the task is not to predict an end state, but to recognise that the era of effortless monetary hegemony has given way to one of careful balance.

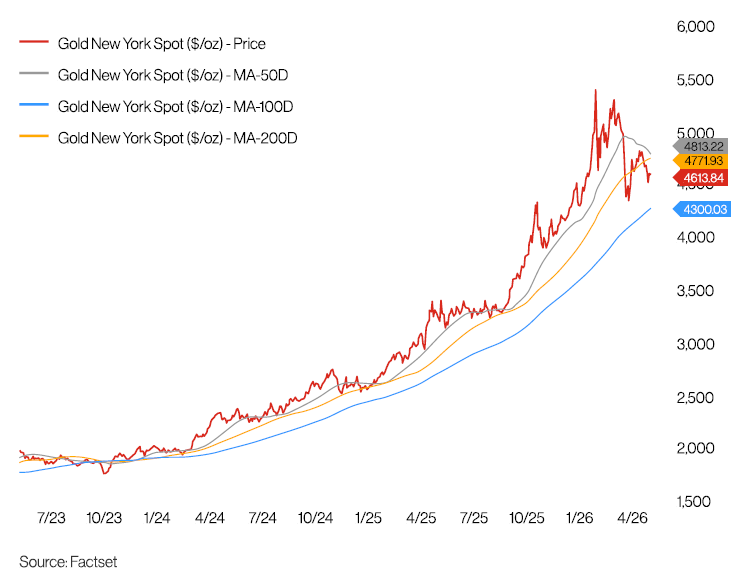

In our Global balanced portfolios, we continue to advocate for a tactical overweight allocation in Gold. Gold is going through a consolidation phase that, on closer inspection, looks more like an entry point than a warning sign. The metal is still trading roughly 15% below its January peak (Figure 7), even as US equity indices post new records. A divergence that reflects less a challenge to the structural thesis than a tactical repositioning in an environment of elevated rates and improved risk sentiment.

Figure 7: Gold trading below January peak

Disclaimer

This material is for the use of the recipient in accordance with the restrictions and/or limitations implemented by any applicable laws and regulations only. It is intended only for the recipient and may not be published, circulated, reproduced or distributed in whole or in part to any other person without the Bank’s prior written consent. Unless otherwise indicated, the information is made available for informational purposes only, without considering the recipient’s financial situation, investment objectives, risk tolerance, financial situation, or any other particular needs and should not be treated as legal or taxation advice.

The information is not and should not be construed as an offer or a solicitation to deal in any investment product or to enter into any legal relations. Any investment decision made based on the information provided is the sole responsibility of the client. The Bank disclaims any liability for any losses or damages resulting from the use of this information. The Bank assumes no responsibility for the way in which the client may choose to use or apply this information, or for any investment decision or transaction that the client might undertake as a consequence. It is the client’s own responsibility to ensure that this product is suitable for him or her and the client must make his or her own decision concerning this product. The client may also wish to obtain advice from other sources before making any decision.

Past performance is not indicative of future results. Any forecast on the economy, stock market, bond market and economic trends of the markets are not necessarily indicative of the future or likely performance of the product. Any investment involves risks, including the total loss of the invested capital.

For queries arising from, or in connection with this material, please contact the person who sent you this material. This advertisement has not been reviewed by the Monetary Authority of Singapore.