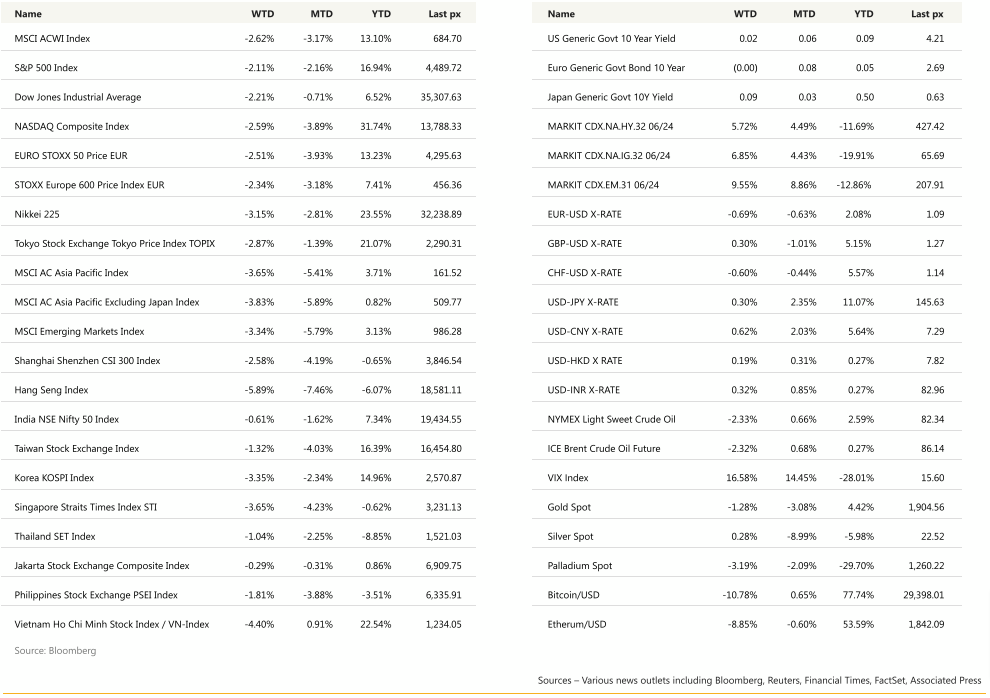

US Tech recorded its worst weekly losing streak this year as higher longer term yields and Chinese economic challenges weighed on overall sentiment. US stocks recorded its 3rd consecutive week of losses as good news still spelled bad news for risk assets.

Retail sales, housing starts and industrial production data all beat expectations. Resilience in the US have spurred bets that the Fed could keep rates higher for longer and any cuts keep getting pushed back. The US 10-year Treasury yield rose to its highest level since November at 4.25% whilst the 2-year was less volatile, remaining below 5% which it briefly pierced earlier in the week. Goldmans is the latest to officially “pencil in” a rate cut in Q2 of 2024. The last FOMC minutes showed officials saw “significant” upside risks to inflation and considered further rate increases although a couple of members preferred a pause to allow the cumulative effects of rate hikes unwind into the broader economy. But overall, our read on the minutes weren’t all that surprising given Powell’s post-meeting press conference. The “significant” element in our view, appears relative when multiple indicators are pointing to disinflationary processes in place. This week will see S&P US Global manufacturing, services, composite readings together with U. of Mich. Sentiment and inflationary expectations.

The major event for the week is Wyoming’s Jackson Hole symposium. Observers are split with what Powell may allude to. One camp (c. DB) says the Fed is comfortable with higher rates as recent data suggests US economic growth is too strong whilst the other says the Fed cant really afford to see this yield keep going up so, they need to calm bond markets down (c. Yardeni). The most likely outcome would be Powell striking a more balanced tone perhaps hinting at the tightening’s end while reinforcing the need to hold rates higher for longer.

Risk-off sentiment kept the USD on its front foot, pressuring precious metals and cryptos. Taking advantage of USD strength to selectively build up Euro and Gold longs.