The Senate overwhelmingly passed bipartisan legislation Saturday (Washington) to avoid a disruptive US government shutdown, sending the bill to President Joe Biden for his expected signature just hours before a midnight deadline. The bill passed on an 88-9 vote.

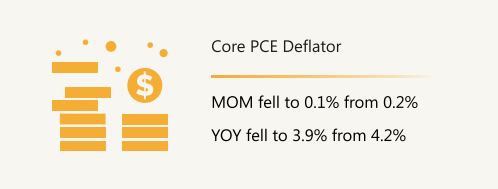

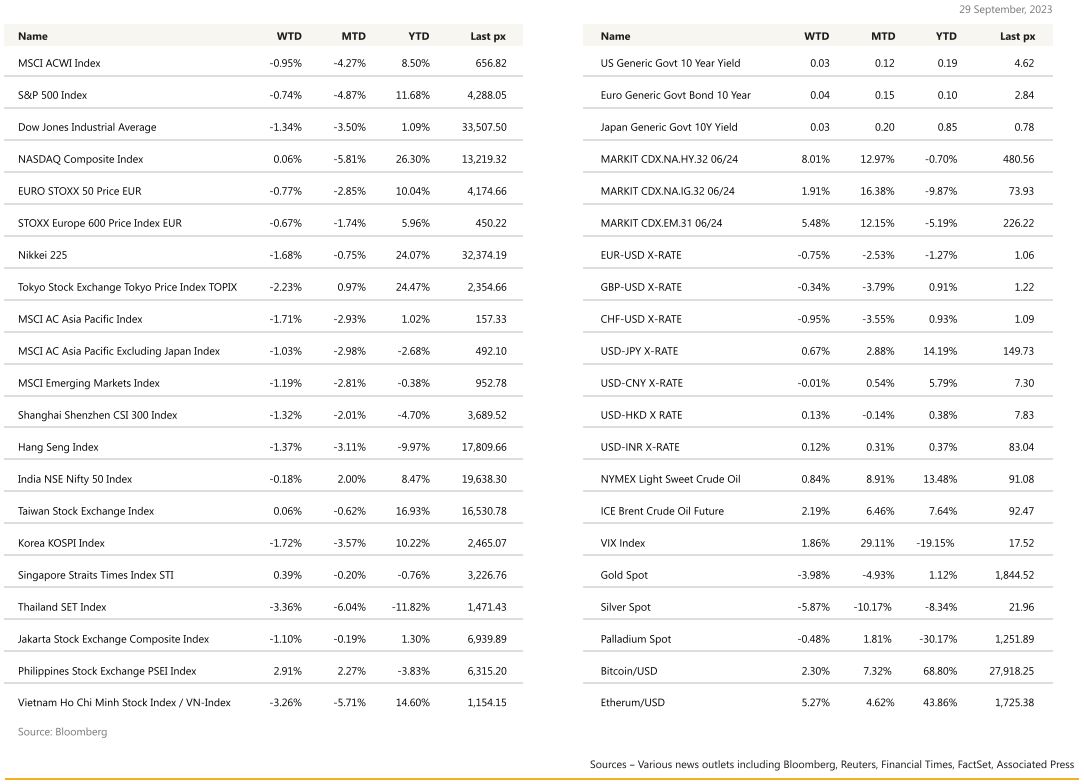

US markets continued its down streak posting its biggest monthly drop of 2023, and the worst quarter since September 2022 on concerns about the Fed Reserve’s policy path in spite of signs of cooling in a key inflation gauge. The Fed’s preferred measure of underlying inflation pressures, the PCE Deflator, rose at the slowest monthly pace since late 2020, while consumer spending edged up. Core PCE Deflator MoM fell to 0.1% from 0.2% (below expectations) and YoY fell to 3.9% from 4.2% (as expected). Headline PCE which includes volatile food & energy prices came in as expected at 3.5% from a revised 3.4% last month. Personal spending and consumption held up although below expectations indicating the consumer continues to spend. US initial jobless claims showed some tightness in the labor market, with the number of new filings edging up slightly to 204,000 last week supporting consumption. However, with the recently expired student loan holiday and rising energy prices, we expect some of this discretionary spending to crimp. NY Fed’s Williams said the central bank is at or near its peak level of interest rates, though policymakers would keep them high for “some time” to bring inflation down to the central bank’s 2% goal – this was the kicker that sent shares lower in the latter half of Friday. Other Fedspeak included Fed Chicago’s President Austan Goolsbee who said policymakers shouldn’t place too much weight on the traditional economic idea that steep job losses are needed to quell inflation, which he said could lead officials to raising rates too high. Richmond’s Barkin said it’s too soon to know if another rate increase will be needed. Other data of interest was the U. of Mich. Inflation expectations which came in as expected at 3.2% and 2.8% for the 1 year and 5-10 year categories respectively, in spite of higher oil prices. The final GDP annualised release came in at 2.1% – no recession just yet perhaps.

On the S&P 500, Bloomberg Intelligence reported that without the Magnificent 7, the index largely trades at a discount to its pre-pandemic norm.

The autumn selloff, combined with positive EPS revisions, has left nine of 11 sectors below pre-2020 average multiples. Of the M7 shares, Amazon.com Inc. gained after news that it will invest as much as $4 billion in AI-startup Anthropic. Microsoft Corp. lost its only sell rating on Monday as Guggenheim upgraded its view on the software giant to neutral, citing a tailwind from generative artificial intelligence. GAI continues to power on….

In Mexico, Banxico kept its policy rate unchanged at 11.25% in a unanimous decision last Thursday. The hawkish pause emphasis remained on a resilient economy, a tight labor market, and mounting inflation measures that remain complex and that are now finding their way into core inflation. Similarly to other central banks, Banxico delivered a hawkish statement stating that it is warranted to keep the policy rate at this level for an extended period of time. The market is now pricing a shallower easing cycle next year, with the policy rate near 10% by EOY. While the probability of Banxico resuming hikes looks low, any further tightening from the Fed will add pressures to Mexican policymakers to keep rates unchanged for longer. This week will see the release of ISM data, factory orders and the key monthly employment data. Unemployment is expected at 3.7% from 3.8% with NFP to fall slightly to 165k from August’s 179k.

On oil, we recognise the expected lags in performance of oil companies in spite of crude’s ascend up 12.15% ytd. Opportunistically, we see potential for some upside for Chevron which is down 6.06% ytd, Conoco Phillips which is up 1.53% and Occidental up 3% ytd.