/ Monthly Market Update - April 2026

The Board of Peace: Is it what it's supposed to be?

“It's good until it's not, it works until it doesn't.”

- Barbara Ann Webber, a former Credit and Financial Analyst, March 2018.

Table of Contents

Insights

Insights

So, what exactly is the Board of Peace?

We have all seen snippets of it on main media streams, glanced over mentions of it in print and, mostly dissing it as yet another Trump distraction.

BUT….

Let us deep dive a little into it – there actually may be some substance to it.

What the Board of Peace Is and Why It Matters in Today’s Geopolitical System

The Board of Peace is a newly-created international organisation that emerged in early 2026 against the backdrop of the Gaza ceasefire and reconstruction effort. While early media coverage often framed it as another short lived political initiative, a closer examination suggests it represents a more substantive – and unconventional – experiment in international governance.

Formally established in January 2026 and welcomed by UN Security Council Resolution 2803 in November 2025, the Board originated as a coordinating mechanism for Gaza’s post war administration and reconstruction. Importantly, the UN resolution did not mandate the Board nor grant it universal authority.

Instead, it acknowledged the Board as a transitional and coordinating body operating outside the formal UN system. This distinction is central to understanding both the Board’s potential strengths and its inherent limitations.

Although Gaza was the catalyst, the Board’s final charter articulates a much broader ambition. It positions the institution as a standing peace building body capable of operating across multiple conflict and post conflict zones, rather than as a single issue vehicle tied exclusively to Gaza. In this sense, the Board is best understood not as a UN substitute, but as a parallel structure designed to bypass some of the procedural and consensus constraints that characterise traditional multilateral institutions.

How the Board Operates: Governance Structure, Power Dynamics and Regional Influence

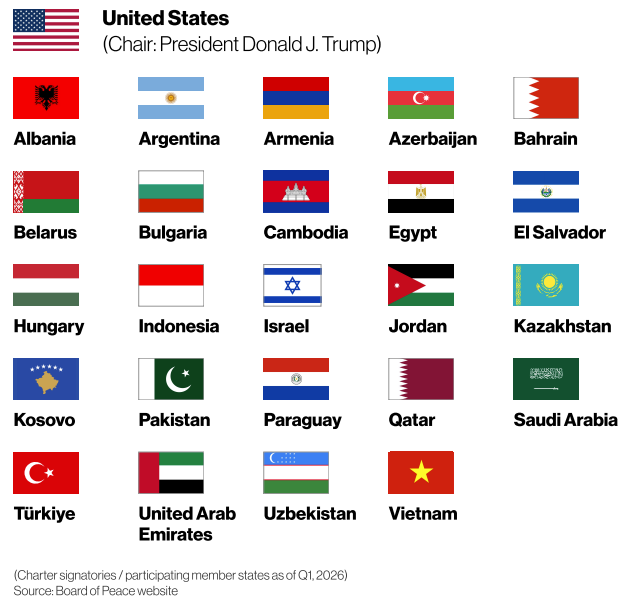

At the core of the Board’s design is an explicitly centralised governance model. The organisation is chaired in perpetuity by U.S. President Donald J. Trump, with the Chair holding extensive authority, including the power to invite or exclude members, approve or veto resolutions, and break voting ties. Membership is by-invitation only and structured around two tiers: permanent members, who secure long term participation through a USD 1 billion capital contribution, and term members, who serve renewable three year mandates. By early 2026, roughly 25 states had signed the charter out of approximately 60 invited.

From a policy perspective, this architecture represents a clear departure from consensus driven multilateralism. Decision making authority is deliberately concentrated, with speed and decisiveness prioritised over broad representation. At the same time, the Board introduces a capital anchored model of participation, linking geopolitical influence directly to financial commitment. In practice, this has enabled the rapid mobilisation of multi billion dollar pledges for reconstruction and humanitarian support, with the World Bank designated to manage and disburse funds under the Board’s strategic direction.

The Board’s stated mission is threefold: to promote stability, restore dependable and lawful governance, and secure enduring peace in areas affected or threatened by conflict. Operationally, this translates into coordinating post conflict reconstruction and humanitarian funding, supporting transitional governance frameworks, overseeing demilitarisation and security stabilisation, and developing replicable peace building practices. While the initial operational focus remains Gaza, the absence of any geographical limitation in the charter leaves open the possibility of future expansion.

These features make the Board a potentially powerful coordination hub, particularly in environments where political authority, security oversight and capital allocation must move in tandem. In effect, it resembles a “coalition of capital” rather than a traditional rules based multilateral lender. Should it succeed in stabilising target regions, the resulting compression of political risk could have meaningful economic and investment implications.

That said, the Board’s structure has attracted material criticism. The concentration of authority in the Chair raises governance and accountability concerns, while the Board’s parallel existence risks friction with established UN mechanisms and broader multilateral norms. Moreover, the charter’s broad mandate leaves unresolved questions around geographic scope, duration of involvement and exit strategies in post conflict settings.

These tensions are particularly visible in the context of the current Iran war.

The Board of Peace in Current Conflicts: Iran Tensions and Diplomatic Limits

To date, the Board has not functioned as a peace broker between Washington and Tehran. Iran is not a member, does not recognise the Board as neutral, and has publicly rejected claims of direct engagement.

Instead, the Board’s role has been indirect. It has acted as a coordination framework around U.S. ceasefire proposals — notably the recently discussed 15 point framework — and as a mechanism to prevent the Iran conflict from derailing the Gaza stabilisation process entirely.

In parallel, the Board has served as a platform for indirect diplomacy. Its envoys have continued engagement with Hamas in Cairo, while regional member states such as Indonesia, Pakistan, Türkiye, Egypt and Saudi Arabia have used their Board participation as diplomatic cover to pursue mediation channels with Tehran outside the U.S.–Iran bilateral track. In this sense, the Board operates less as a negotiating table and more as a diplomatic clearinghouse.

Looking forward, the most realistic application of the Board to the Iran war lies not in imposing peace, but in structuring de-escalation and managing consequences. Analysts broadly agree that its comparative advantage is in sequencing an off ramp — potentially involving phased ceasefires, conditional sanctions relief, maritime deconfliction in the Strait of Hormuz and commitments to restrain proxy activity.

Should the conflict de escalate or freeze, the Board could then be repurposed as a post-conflict containment and reconstruction body, coordinating humanitarian stabilisation and reducing spillover risks across Iraq, Lebanon, the Gulf and global shipping lanes.

Crucially, there are limits to what the Board can achieve. Embedded within a wartime command environment and closely associated with U.S. leverage, it lacks the neutrality required to act as a trusted mediator in Tehran’s eyes. More fundamentally, it cannot substitute for a domestic political settlement inside Iran. Absent a credible political design, military degradation alone risks regime fragmentation, proxy violence and long term regional instability — challenges that sit beyond the Board’s current remit.

In net terms, the Board of Peace should be viewed as a structural experiment in international governance rather than a conventional peace institution. Its value lies in coordination, capital mobilisation and post conflict sequencing, not in diplomacy for its own sake. For policymakers, it is most useful after peak escalation rather than during active conflict. For investors, its relevance is second order, influencing risk premia, energy volatility and long dated reconstruction optionality more than near term asset pricing.

The Board’s long term significance will ultimately depend on three factors: whether it can deliver tangible results in Gaza, whether member states remain committed as geopolitical conditions evolve, and whether it can coexist (rather than collide with) existing global institutions. Whether it proves a durable innovation or a transient construct remains an open question, but it is no longer credible to dismiss it as mere political theatre.

Taking all of this into account, we think that the Board of Peace can be applied to the Iran war only as a framework for managing consequences and enabling an off ramp, not as a neutral peace broker. Its value lies in what comes after escalation, not in stopping the escalation itself.

What This Means for Markets: Infrastructure, Energy and Reconstruction Opportunities

To this extent, we would be prepared to invest in potential opportunities, in:

- Infrastructure

- Energy logistics

- Utilities and construction materials

This is not a near term trade, but a watch list opportunity, contingent upon:

- A clear de-escalation, and

- Capital deployment via multilateral channels

Appendix 1

Confirmed Member States:

Looking at the list of members, is it any wonder then, why Gulf states have been tolerant of Iran’s continued attacks on their soil…

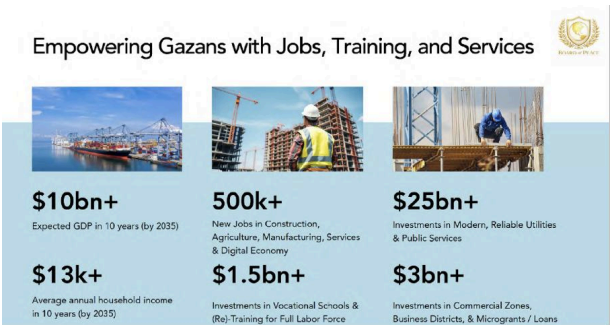

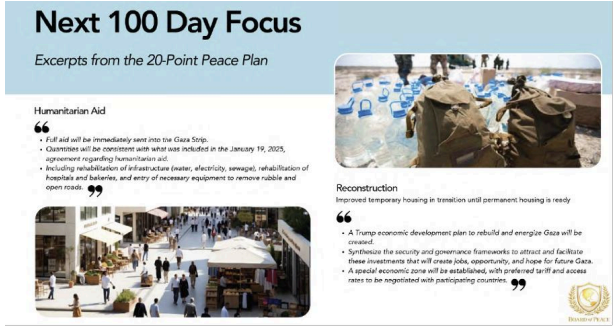

Appendix 2: Extracts of The Charter as presented at the Davos World Economic Forum:

Source: Board of Peace website, https://boardofpeace.org/presentations

Conclusion

A world that is stable – until it isn’t. Bring it on!

Disclaimer

This material is for the use of the recipient in accordance with the restrictions and/or limitations implemented by any applicable laws and regulations only. It is intended only for the recipient and may not be published, circulated, reproduced or distributed in whole or in part to any other person without the Bank’s prior written consent. Unless otherwise indicated, the information is made available for informational purposes only, without considering the recipient’s financial situation, investment objectives, risk tolerance, financial situation, or any other particular needs and should not be treated as legal or taxation advice.

The information is not and should not be construed as an offer or a solicitation to deal in any investment product or to enter into any legal relations. Any investment decision made based on the information provided is the sole responsibility of the client. The Bank disclaims any liability for any losses or damages resulting from the use of this information. The Bank assumes no responsibility for the way in which the client may choose to use or apply this information, or for any investment decision or transaction that the client might undertake as a consequence. It is the client’s own responsibility to ensure that this product is suitable for him or her and the client must make his or her own decision concerning this product. The client may also wish to obtain advice from other sources before making any decision.

Past performance is not indicative of future results. Any forecast on the economy, stock market, bond market and economic trends of the markets are not necessarily indicative of the future or likely performance of the product. Any investment involves risks, including the total loss of the invested capital.

For queries arising from, or in connection with this material, please contact the person who sent you this material. This advertisement has not been reviewed by the Monetary Authority of Singapore.